This content is for Subscriber members only.

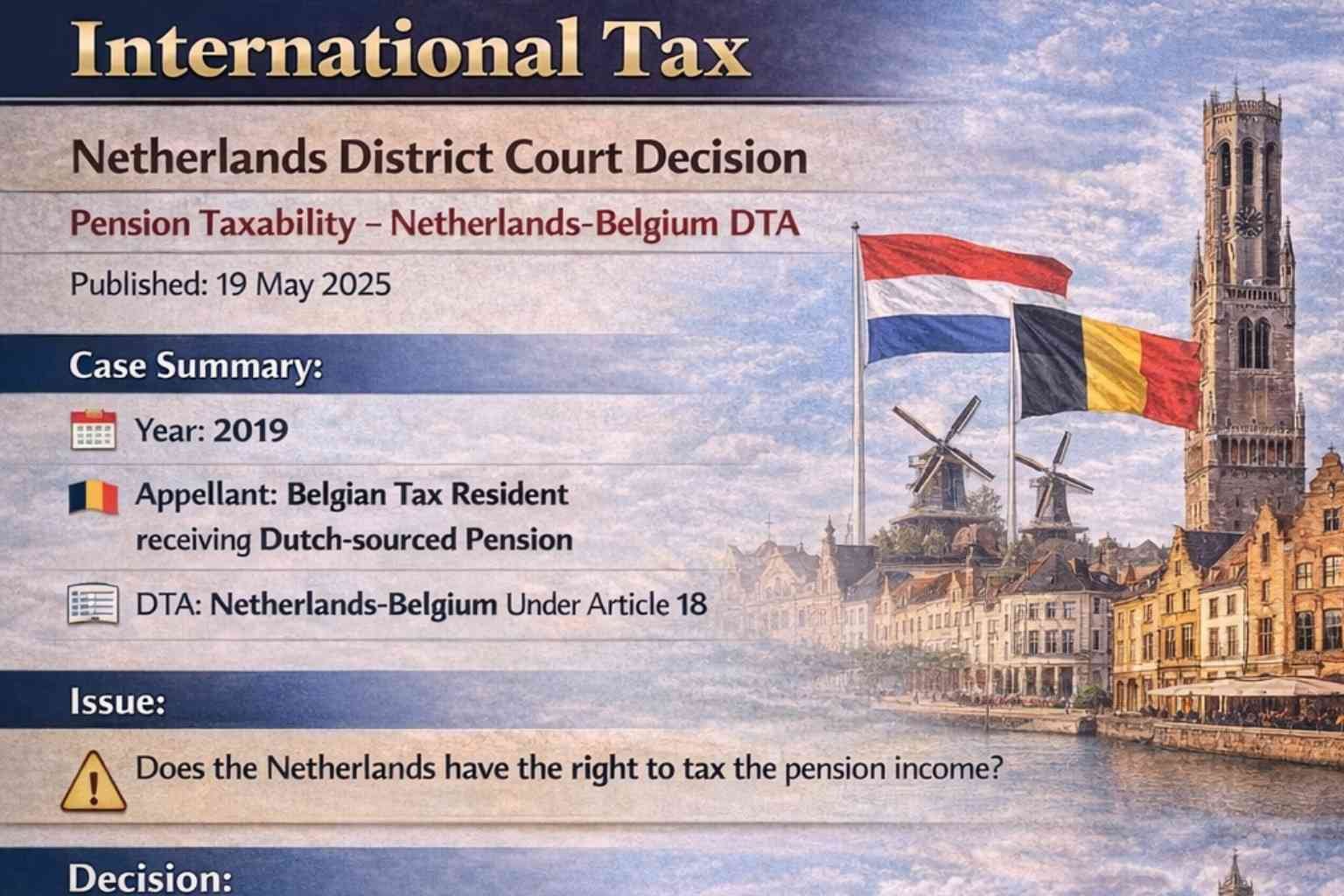

Pension taxability – Netherlands-Belgium DTA

Facts:

In 2019, the appellant was a tax resident in Belgium and received pensions that accrued and originated in the Netherlands based on past duties performed. According to Article 18 of the Double Taxation Agreement (DTA), the primary right to tax the pension lies with the state of residency. However, the pension may also be taxed in the state of origin under two conditions:

- The pension contributions were deducted when they accrued for computing taxable income in the state of origin, or any tax relief was applicable to the pension contributions.

- The pension income in the current year is not taxed at the generally applicable rate in the state of residence, specifically for non-self-employed occupations, or less than 90% of the gross pension income is included for taxation purposes.

Part of the pension income was progressively taxed in Belgium in the current year, while the other part was not. Condition (b) would be satisfied if the pension income was not progressively taxed in Belgium.

The revenue authorities contended that the entire pension income was taxable in the Netherlands as condition (a) above was satisfied.

Issue:

Whether the Netherlands has the right to tax the pension income, and if so, to what extent.

Decision:

The court ruled, based on Article 18(2), that the Netherlands has the right to tax up to the amount for which pension income accrued in a tax-facilitated manner (deducted from taxable income in the years of accrual – condition (a)), and up to the amount for which the benefits are not progressively taxed in Belgium (condition (b)). In other words, the court rejected the revenue’s contention and clarified that the Netherlands will have the right to tax only when both conditions (a) and (b) are satisfied.

Based on the facts, the court decided that both conditions were satisfied concerning the part of the pension income that was not progressively taxed in Belgium. Accordingly, that part of the pension would be taxable in the Netherlands.

Key Takeaways:

Regarding condition (a) above, the appellant claimed that part of their pension income was not deducted for taxation in the Netherlands. However, appellant could not provide documentary evidence. Therefore, it is critical to save all employment contracts, payslips, and filed income tax returns from where duties were performed for situations like these.

#InternationalTax