Facts:

A Dutch funeral insurance company, whose parent moved to Luxembourg in 2015, planned a business divestment through demerger in 2017. The company sought advance approval for tax exemption under Article 14a(2) of Dutch corporation tax law (CITA). The Inspector denied this, arguing insufficient evidence that the transaction wasn’t primarily tax driven. Lower courts agreed, applying Article 14a(6)’s statutory presumptions against the taxpayer.

Note:

Article 14a(2) CITA provides tax neutrality for demerger and Art. 14a(6) provides for Anti‑avoidance provisions as below:

- First sentence (substance test): the exemption does not apply if the demerger is predominantly aimed at avoiding or deferring tax.

- “General presumption” (second sentence): where a demerger lacks commercial reasons, it is presumed avoiding or deferring tax unless the taxpayer shows otherwise.

- “Second presumption” (last sentence; 3‑year rule): if shares in the divided or acquiring entity are transferred to an unrelated party within three years, commercial reasons are deemed absent unless rebutted.

Under the EU Merger Directive (Articles 4 & 15), member States may deny relief where the main purpose (or a main purpose) is tax avoidance; lack of commercial reasons creates only a rebuttable, case‑specific presumption, not a general suspicion.

Legal Issue:

The key issue was whether Article 14a(6) CITA, specifically its presumption that a demerger lacks commercial reasons when shares are sold within three years, is compatible with Article 15 of the EU Merger Directive. The question was whether the Court of Appeal apply an unlawful burden‑of‑proof rule by treating the statutory presumption as a general suspicion of tax avoidance?

Revenue Inspector’s Arguments:

- The taxpayer failed to show that the demerger had genuine commercial reasons; business motives claimed were unsubstantiated.

- The advantages cited over an asset‑liability deal were not demonstrated in practice and likely marginal compared to tax benefits.

- The step‑plan was an artificial structure whose primary purpose was to achieve a tax‑facilitated transfer.

- Sale of the new company’s share to a third party within three years triggered statutory presumption of no commercial motives.

- Overall transaction intended predominantly to avoid or defer corporate income tax.

Supreme Court’s Analysis

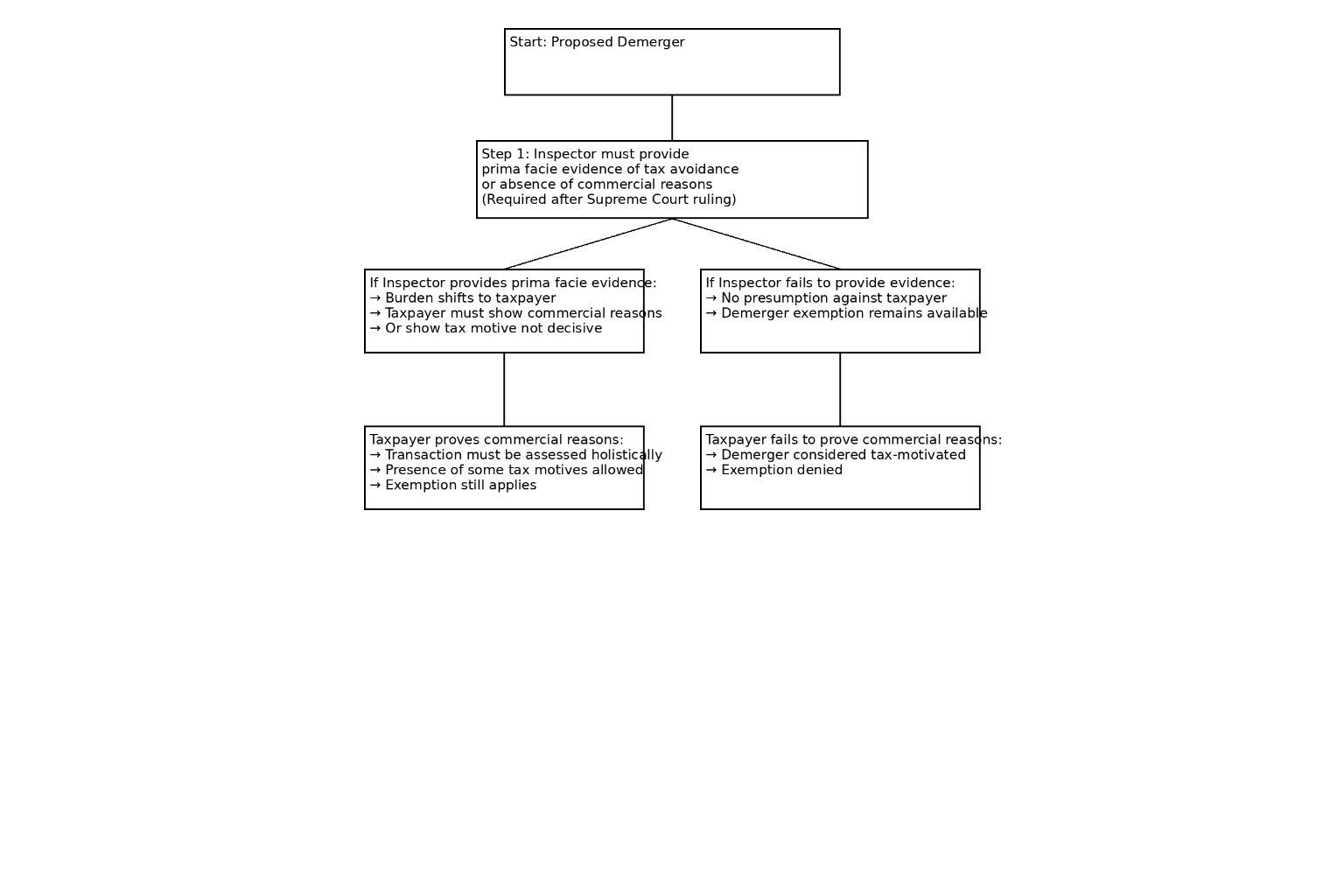

The Supreme Court held that the Court of Appeal incorrectly applied the burden‑of‑proof system in Art. 14a(6) CITA. The Court emphasized that Art. 14a must be interpreted in conformity with the EU Merger Directive, which permits only a case‑specific presumption of avoidance and prohibits general or automatic presumptions.

The statutory rule that commercial reasons are “deemed absent” when shares are sold within three years (the second presumption) operates as a general suspicion of tax avoidance, shifting the entire burden to the taxpayer without requiring the Inspector to provide prima facie evidence. This contradicts Art. 15 of the Merger Directive and EU case law requiring authorities to first show objective indications of tax‑avoidance purpose.

Because the Inspector provided no prima facie evidence, the presumption could not arise, and the burden could not shift. The Court of Appeal’s reasoning that treating the presumption as automatically applicable was thus rested on an unlawful burden allocation. Therefore, all findings based on that presumption must be set aside. The case must be reconsidered with the correct rule:

- Inspector must first show prima facie evidence of tax‑avoidance motive or absence of commercial reasons.

- Only then may the burden shift to the taxpayer to show commercial motives or that tax motives were not decisive.