This content is for Subscriber members only.

Background and our understanding

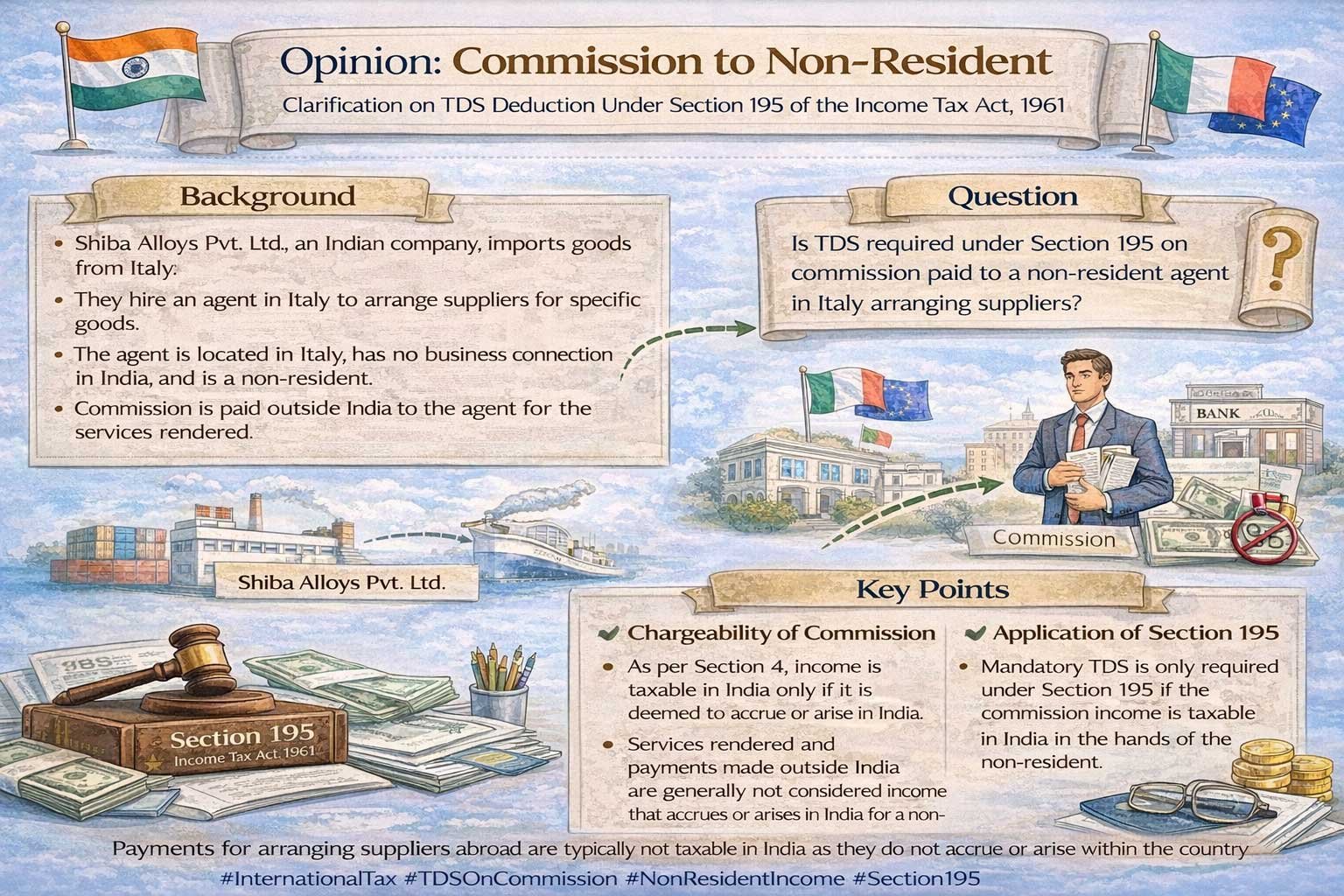

- As per our telephonic discussion, we understand that Shiba Alloys Pvt Ltd (Hereinafter referred to as the “company”) requires certain goods from Italy to be imported in India in order to manufacture specific products here in India.

- For the above purpose, company has approached an agent in Italy who will make arrangements to deal with different suppliers of the goods their which company wants to import. The agent will be entitled to receive commission from the company for providing aforesaid service.

- It is assumed that the agent is based at Italy and has no business connection in India through any branch, subsidiary, liaison office, project office in India.

- It is assumed that the agent is a non-resident as per section 6 of the Act

- It is also assumed that the payment of commission will be made outside India i.e. amount will be transferred in a bank account outside India.

Clarification required by the company

- Is it required to deduct TDS on payment of commission to the agent in Italy for the services rendered by him outside India under section 195 of the Act?

Understanding the provisions of the Act

- Section 4 of the Act is the chargeability section which empowers the Income Tax Authorities to levy tax on the total Income of all persons at the rate applicable for such year. Relevant extract of section 4 is produced here below for better understanding:

“4. (1) Where any Central Act enacts that income-tax shall be charged for any assessment year at any rate or rates, income-tax at that rate or those rates shall be charged for that year in accordance with, and 1[subject to the provisions (including provisions for the levy of additional income-tax) of, this Act] in respect of the total income of the previous year 2[* * *] of every person

:Provided that where by virtue of any provision of this Act income-tax is to be charged in respect of the income of a period other than the previous year, income-tax shall be charged accordingly.

(2) In respect of income chargeable under sub-section (1), income-tax shall be deducted at the source or paid in advance, where it is so deductible or payable under any provision of this Act”

- If we look at sub section (2) above, it shifts responsibility on the payer to deduct TDS on payment of any amount which constitutes income chargeable to tax in India in the hands of recipient under sub-section (1) above. Therefore in this case if the payment of commission by the company to the agent is chargeable to tax in India in the hands of agent then only company is responsible to deduct TDS. Therefore now we need to understand what are all the income which can be brought to tax in the hands of non-resident. For this purpose, it is pertinent here to analyse the words/phrase “Total Income” as stated in sub section (1) above.

- “Total income” is defined in section 2(45) of the Act which states that total income means income as per the scope defined under section 5 of the Act which is computed according to the provisions of the Act.

- Now we will move to section 5 of the Act to understand the scope of total Income. As the agent in this case is a non-resident, it is needed to know what are all the incomes which can be brought to tax in India in his hands i.e. the scope of total income in the hands of non-resident which has been defined in section 5(2) of the Act. Section 5(2) states the following incomes shall be taxable in India for non-residents:

- Income received in India or deemed to be received in India

- Income accrue or arise in India or deemed to accrue or arise in India.

- Point (a) above is not relevant in this case as it has been already assumed that the payment is made outside India. Further it cannot be said that income accrue or arise in India as the services have been performed outside India and right to receive the Income is also generated outside India. Therefore now it is important to analyse whether any income fall under the scope of “Income deemed to accrue or arise in India” which has been defined in section 9 of the Act. Section 9 broadly includes following incomes:

- all income accruing or arising, whether directly or indirectly, through or from any business connection in India or

- through or from any property in India or

- through or from any asset or source of income in India or

- through the transfer of a capital asset situate in India

- Income from salary if it is earned in India.

- Income chargeable under the head “Salaries” payable by the govt. To a citizen of India for services outside India.

- A dividend paid by Indian company outside India.

- Income by way of Interest

- Income by way of royalty

- Income by way of fees for technical services.

- The nature of Income in the hands of agent in our case is commission which is a business income in his hands. Therefore nature of Income listed above from point (b) to (j) is not applicable at all. Only point (a) may be applicable if and only if the agent has any business connection in India. This we have already assumed earlier in this note that the agent does not have any business connection in India. For the sake of understanding, the definition of “Business Connection” which is defined in explanation 2 to section 9(1) of the Act, is produced here below:

“Explanation 2.—For the removal of doubts, it is hereby declared that “business connection” shall include any business activity carried out through a person who, acting on behalf of the non-resident,—

(a) has and habitually exercises in India, an authority to conclude contracts on behalf of the non-resident, unless his activities are limited to the purchase of goods or merchandise for the non-resident; or

(b) has no such authority, but habitually maintains in India a stock of goods or merchandise from which he regularly delivers goods or merchandise on behalf of the non-resident; or

(c) habitually secures orders in India, mainly or wholly for the non-resident or for that non-resident and other non-residents controlling, controlled by, or subject to the same common control, as that non-resident:

Provided that such business connection shall not include any business activity carried out through a broker, general commission agent or any other agent having an independent status, if such broker, general commission agent or any other agent having an independent status is acting in the ordinary course of his business :

Provided further that where such broker, general commission agent or any other agent works mainly or wholly on behalf of a non-resident (hereafter in this proviso referred to as the principal non-resident) or on behalf of such non-resident and other non-residents which are controlled by the principal non-resident or have a controlling interest in the principal non-resident or are subject to the same common control as the principal non-resident, he shall not be deemed to be a broker, general commission agent or an agent of an independent status”

- As the agent has no business connection in India, it is not falling under point (a) also. Therefore this commission income in the hands of agent is also not coming under the scope of “Income deemed to accrue or arise in India”. Accordingly section 5 is failed to include any income in the hands of non-resident agent in this case which in result fails section 4 of the Act.

- On the basis of above it can be concluded that this commission Income is not chargeable to tax in India in the hands of non-resident agent and therefore there is no liability in the hands of the company to deduct TDS on payment of such commission.

- It may not be out of place to note that section 195 of the Act also points out that TDS on payment of any sum to a non-resident is required to be deducted if the amount paid is chargeable to Tax in India in the hands of recipient of such sum. Therefore question of deducting TDS comes into picture only when the amount paid is taxable in India in the hands of recipient. For the sake of proper understanding, relevant extract of section 195 has been produces here below:

“195. 1[(1) Any person responsible for paying to a non-resident, not being a company, or to a foreign company, 17[any interest (not being interest referred to in section 194LB or section 194LC)] 20[or section 194LD] 2[***] or any other sum chargeable under the provisions of this Act (not being income chargeable under the head “Salaries” 3[***]) shall, at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier, deduct income-tax thereon at the rates in force”

- As the commission Income is not chargeable to tax in the hands of non-resident agent as discussed earlier in this note, liability under section 195 of the Act does not arise.

Brief reference of judicial pronouncements under Income Tax Law

- Please note that in various cases, it has been held that income from any services provided by the non-resident outside India which does not have any business connection in India, would not be taxable in India. In the case of Commissioner of Income Tax v. Toshoku Limited (1980) 125 ITR 525, supreme court has held as under:

“While dealing with Section 9(1) of the Act, the Supreme Court in Commissioner of Income Tax v. Toshoku Limited, (1980) 125 ITR 525, on considering a transaction where tobacco was exported to Japan and France and sold through non-resident assessees who were paid commission, held as under: ‘8. The second aspect of the same question is whether the commission amounts credited in the books of the statutory agent can be treated as incomes accrued, arisen, or deemed to have accrued or arisen in India to the non-resident assessees during the relevant year. This takes us to s. 9 of the Act. It is urged that the commission amounts should be treated as incomes deemed to have accrued or arisen in India as they, according to the department, had either accrued or arisen through and from the business connection in India that existed between the non-resident assessees and the statutory agent. This contention overlooks the effect of cl. (a) of the Explanation to cl. (i) of sub-s. (1) of s. 9 of the Act which provides that in the case of a business of which all the operations are not carried out in India, the income of the business deemed under that clause to accrue or arise in India shall be only such part of the income as is reasonably attributable to the operations carried out in India. If all such operations are carried out in India, the entire income accruing therefrom shall be deemed to have accrued in India. If however, all the operations are not carried out in the taxable territories, the profits and gains of business deemed to accrue in India through and from business connection in India shall be only such profits and gains as are reasonably attributable to that part of the operations carried out in the taxable territories. If no operations of business are carried out in the taxable territories, it follows that the income accruing or arising abroad through or from any business connection in India cannot be deemed to accrue or arise in India (See CIT v. R. D. Aggarwal and Co. [1965] 56 ITR 20 (SC) and Carborandum Co. v. CIT [1977] 108 ITR 335 (SC) which are decided on the basis of s. 42 of the Indian I.T. Act, 1922, which corresponds to s. 9(1)(i) of the Act). 9. In the instant case, the non-resident assessees did not carry on any business operations in the taxable territories. They acted as selling agents outside India. The receipt in India of the sale proceeds of tobacco remitted or caused to be remitted by the purchasers from abroad does not amount to an operation carried out by the assessees in India as contemplated by cl. (a) of the Explanation to s. 9(1)(i) of the Act. The commission amounts which were earned by the non-resident assessees for services rendered outside India cannot, therefore, be deemed to be incomes which have either accrued or arisen in India. The High Court was, therefore, right in answering the question against the department”.

- Further in the Landmark case of GE India Technology Centre Pvt Ltd Vs CIT 327 ITR 456, has held that it is not required to deduct TDS on payment to non-resident if the same is not chargeable to tax in India in the hands of non-resident.

- In the case of The Commissioner of Income Tax Versus Kikani Exports Pvt. Ltd 369 ITR 96, Madras High Court has held that the assessee is not liable to deduct tax at source when the non-resident agent provides services outside India on payment of commission. Here in this case assessee has engaged a selling agent outside India for sale of exported goods. It has also been held that the same income cannot be treated as fees for technical services and can at best be called as a service for completion of the export commitment..

Conclusion

- Thus, in our opinion, TDS is not required to be deducted under section 195(1) of the Act for payments of commission to non-resident agent for the services provided by him outside India.