This content is for Subscriber members only.

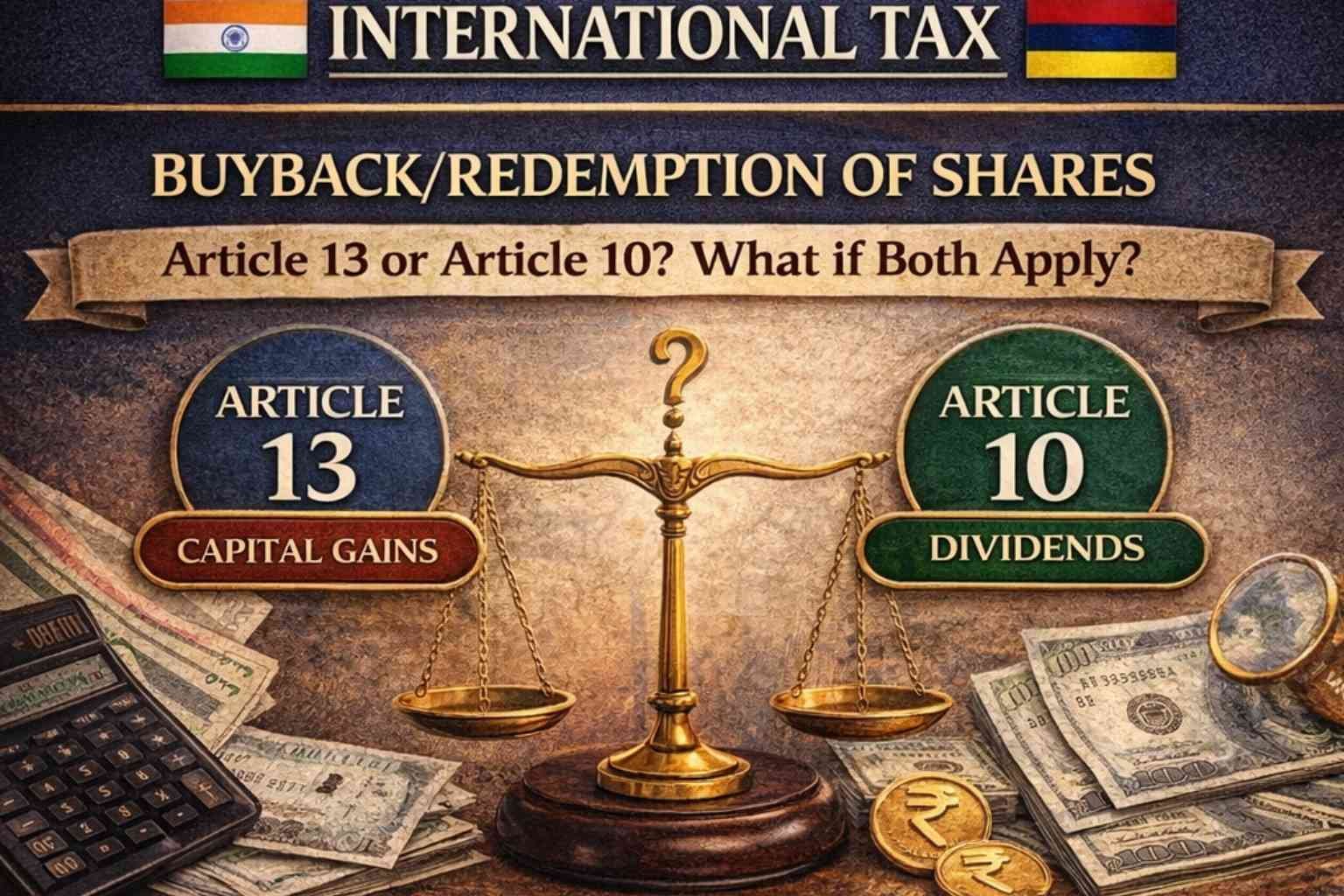

Article 13 or Article 10? What if both articles Apply?

I recently had an engaging conversation with a colleague (on a case) about the tax treatment of an Indian company’s share buyback from a non-resident individual. The primary question was whether Article 13 and/or Article 10 of the applicable tax treaty would apply to such transactions.

Under Indian Income Tax Law, effective 1st October 2024, the buyback of shares is treated as a dividend and taxed accordingly in India. Therefore, if an Indian company buys back shares from a non-resident individual, the amount is considered a dividend in the hands of the non-resident and taxed under Indian law. Typically, the Indian company would withhold tax at the time of distribution by applying Article 10 of the relevant tax treaty between India and the non-resident’s jurisdiction.

It should be noted that few treaties with India specify under Article 13 that gains from the alienation of shares are taxable only where the shareholder is resident. As a result, non-resident individuals may seek to apply Article 13 where this provides a more favorable outcome. This raises the key issue of whether Article 10 or Article 13 applies, or potentially both.

In most Indian treaties, Article 10 would generally apply, as it often refers back to domestic law to determine if a payment qualifies as a dividend. Since Indian law treats buybacks as dividends, Article 10 is typically invoked. However, Article 13 in many treaties could also be relevant, as the transaction involves alienation of shares.

To resolve this overlap, OECD and UN commentaries indicate that if redemption of shares is taxed in the source country as a dividend, Article 10 should apply exclusively, not Article 13. Although there may be technical differences between “redemption” and “buyback,” however in my view, under the context of the treaty, buybacks may fall under the same category. Refer para 28 of OECD commentary on article 10 and Para 31 of commentary on article 13.

Therefore, based on current guidance, when India taxes the buyback of shares as a dividend, Article 10 of the treaty applies. Caution is advised for non-resident individuals considering reliance on Article 13 for a more favorable tax treatment, as the prevailing interpretation supports taxation under Article 10 in such cases.

If the jurisdiction of residence of the non-resident individual treats the buyback of shares as a capital gains transaction, based on the OECD and UN commentaries, the jurisdiction of residence is required to provide relief under Article 23A or Article 23B of the Treaty with India. In such instances, taxation by India would be governed in accordance with the provisions of the treaty.

If OECD or UN commentary is absent, a buy-back transaction may fall under both Article 10 and Article 13. The Netherlands Court of Appeal (2 October 2025) decided that if a transaction fits two Convention articles, the provision more favourable to the taxpayer should apply. ECLI:NL:GHSHE:2025:2121

#InternationalTax