This content is for Subscriber members only.

PE profit computation, an interesting scenario – Netherland-Belgium DTA

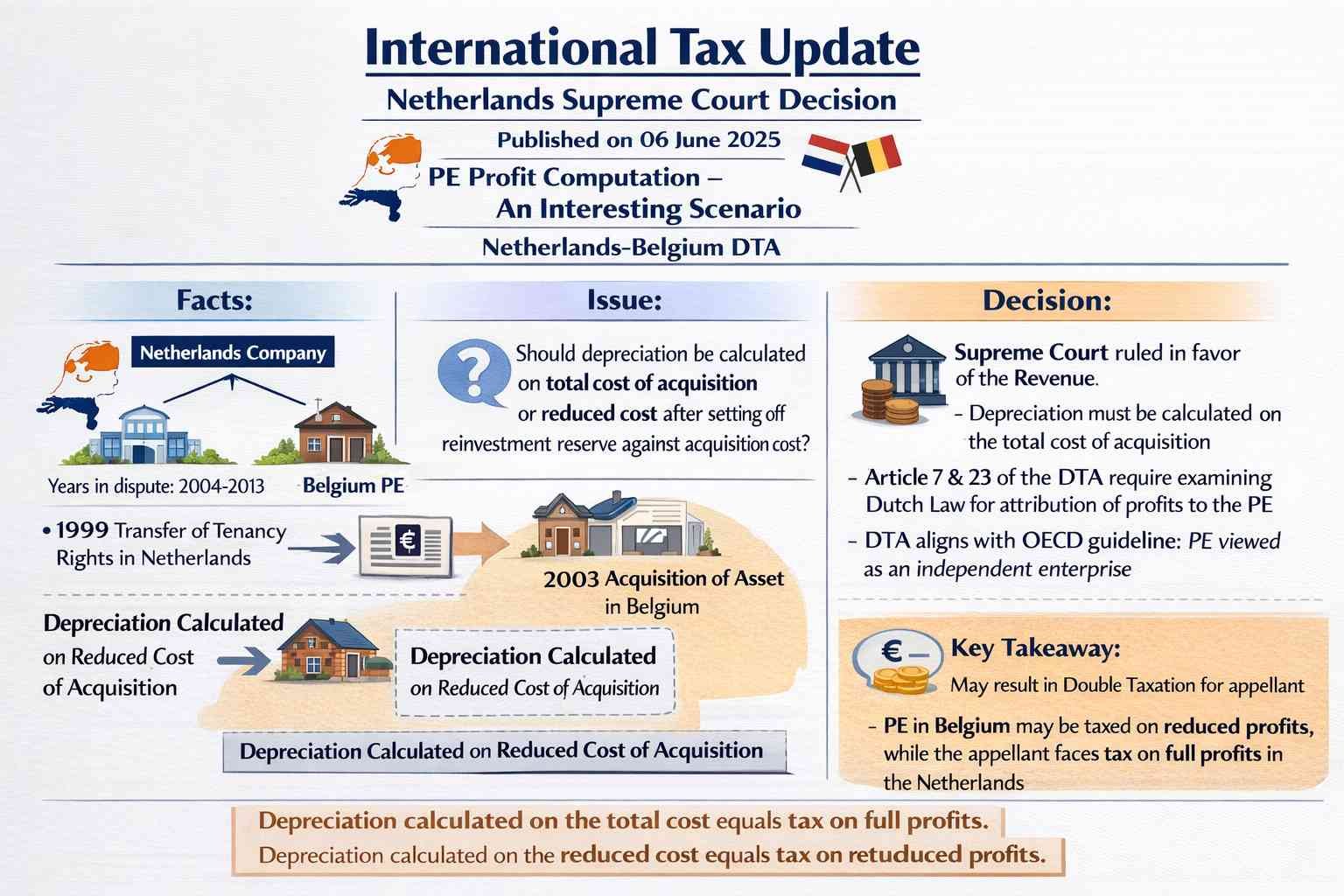

Facts:

The appellant is a company incorporated in the Netherlands with a permanent establishment (PE) in Belgium. The years in dispute are 2004 to 2013. In 1999, the appellant transferred tenancy rights in a supermarket established in the Netherlands. The profits from this transfer were credited to the reinvestment reserve account in the company’s balance sheet. In 2003, the company acquired an asset (right of use of a house) located in Belgium and attributed this asset to the PE in Belgium.

The company set off the reinvestment reserve against the cost of acquisition of the asset in the company’s balance sheet. Depreciation was calculated based on the resulting cost of acquisition (after setting off the reinvestment reserve) to compute the PE profit. According to the Double Taxation Avoidance Agreement (DTA) between Belgium and the Netherlands, the profits of the PE were exempt in the Netherlands.

Issue:

The revenue argued that depreciation should be calculated on the total cost of acquisition of the asset (before setting off the reinvestment reserve) to compute the profits of the PE. Since depreciation was computed on the reduced cost, excess profit was exempted in the hands of the appellant. The district court’s decision favoured the Revenue.

Decision:

The Supreme Court decided the case against the appellant and agreed with the decision of the District Court by establishing the following principles:

- Article 7 read with Article 23 of the DTA requires examination of the domestic law of the Netherlands for attribution of profits to the PE and avoidance of double taxation. Netherlands law mandates viewing the PE as an independent enterprise, consistent with OECD principles.

- The profits of the PE should be computed separately from the profits of the Netherlands business for corporate tax purposes. When determining the profit of the PE to be exempted under a tax treaty, only facts and circumstances relating to the PE are considered. A reinvestment reserve arising from the appellant’s business in the Netherlands does not concern the PE. Therefore, its use is only considered in determining the general taxable profit in the Netherlands, even if the reinvestment reserve has been written off against the purchase price of a replacement asset that became part of the foreign PE’s assets. This means that in calculating the profit of the PE, depreciation of the asset occurs on the acquisition price before the reinvestment reserve is written off.

It was thus decided that the reduced cost of acquisition would be used to compute the profit of only the Netherlands business and not the profit of the foreign PE. Consequently, the excess profit of the PE that was exempted in the hands of the appellant was reduced, and the additional tax determination was upheld.

Key Takeaways:

This decision could result in double taxation for the appellant. Based on this decision, which aligns with OECD guidelines, the PE in Belgium may claim to pay tax on the reduced profits after claiming depreciation as computed according to this decision.

#InternationaTax