This content is for Subscriber members only.

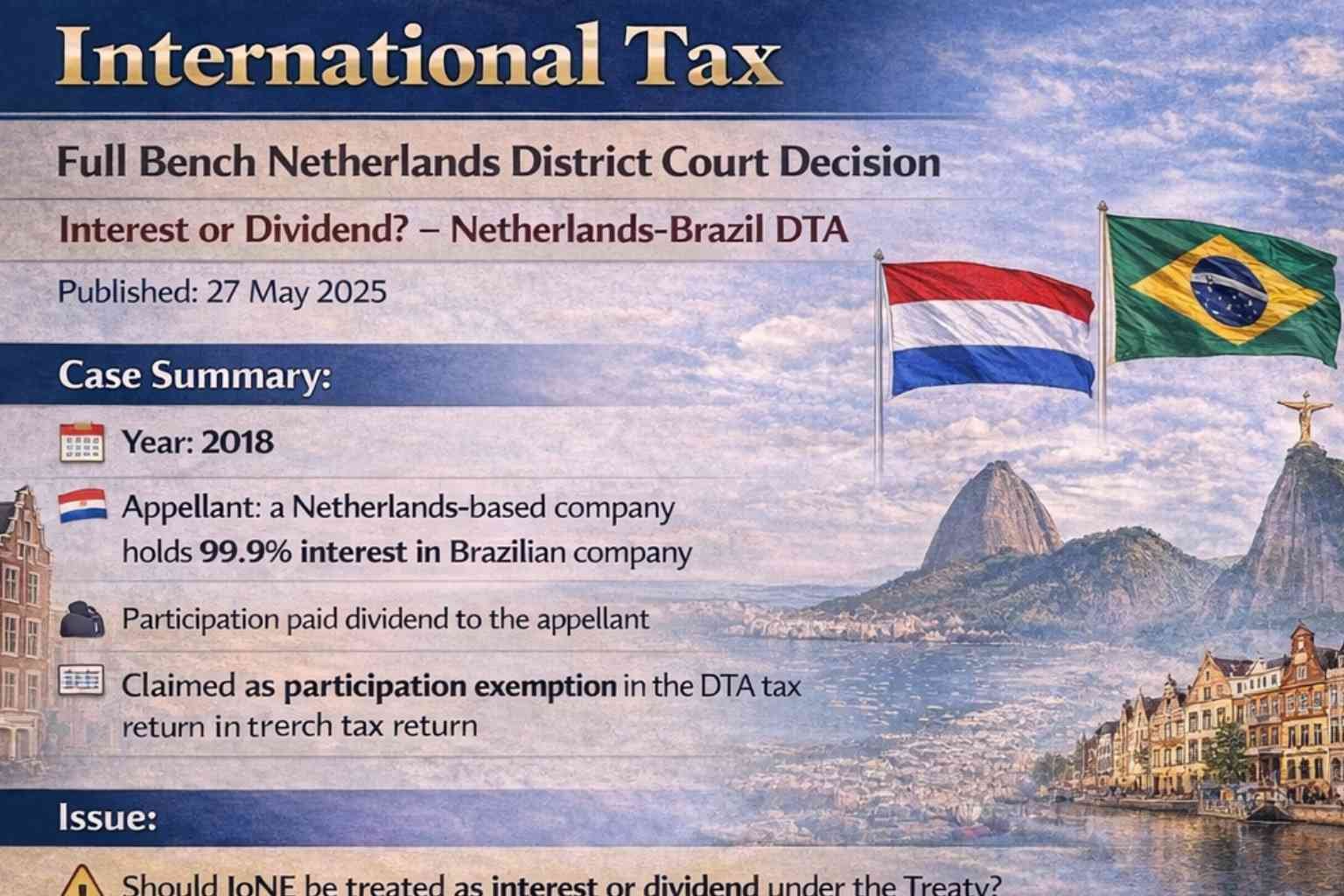

Interest or dividend? – Netherlands-Brazil DTA

Facts:

The appellant, a Netherlands-based company, holds 99.9% interest in a Brazilian company (“Participation”). In 2018, Participation paid dividend to the appellant, claimed as a participation exemption in the Dutch tax return. Additionally, Participation paid ‘juros sobre o capital próprio’ translated into English ‘as Interest on Net Equity’ (IoNE) to the appellant with 15% withholding tax deducted, declared as non-exempt income in the Dutch tax return, claiming a 25% tax sparing credit as per the DTA.

Issue:

Whether IoNE should be treated as interest or dividend under the Treaty. Interest would allow for a 20% tax sparing credit, while dividends would allow for a 25% tax sparing credit.

Note:

The DTA between the Netherlands and Brazil was entered in March 1990 and IoNE was introduced in Brazilian law in 1995. A MAP under article 25 of the treaty in April 2022 clarified that IoNE payments are considered interest under the Treaty.

Revenue’s Argument:

Revenue argues that the text of Articles 10 and 11show the Netherlands and Brazil intended to attach the source state’s classification of the IoNE. In Brazil, this means the IoNE is treated as interest under the treaty. This classification was confirmed by a mutual consultation with Brazil in 2022 based on Article 25.

Court Decision:

The court ruled IoNE payments as dividends, granting a 25% tax sparing credit to the appellant due to the below points:

- IoNE was introduced after the DTA, meaning no classification agreement existed at the time of treaty completion. Thus, Article 3 applies, assigning the meaning of IoNE based on Dutch domestic law, which classifies IoNE as dividends.

- The 2022 MAP does not affect this classification because, under Article 32 of the Vienna Convention, additional interpretations can only clarify existing treaty provisions, not redefine them outside the original joint intention of the Contracting States at the time of completion of the treaty. Therefore, interpretation under MAP could not be applied retroactively.

#InternationaTax