This content is for Subscriber members only.

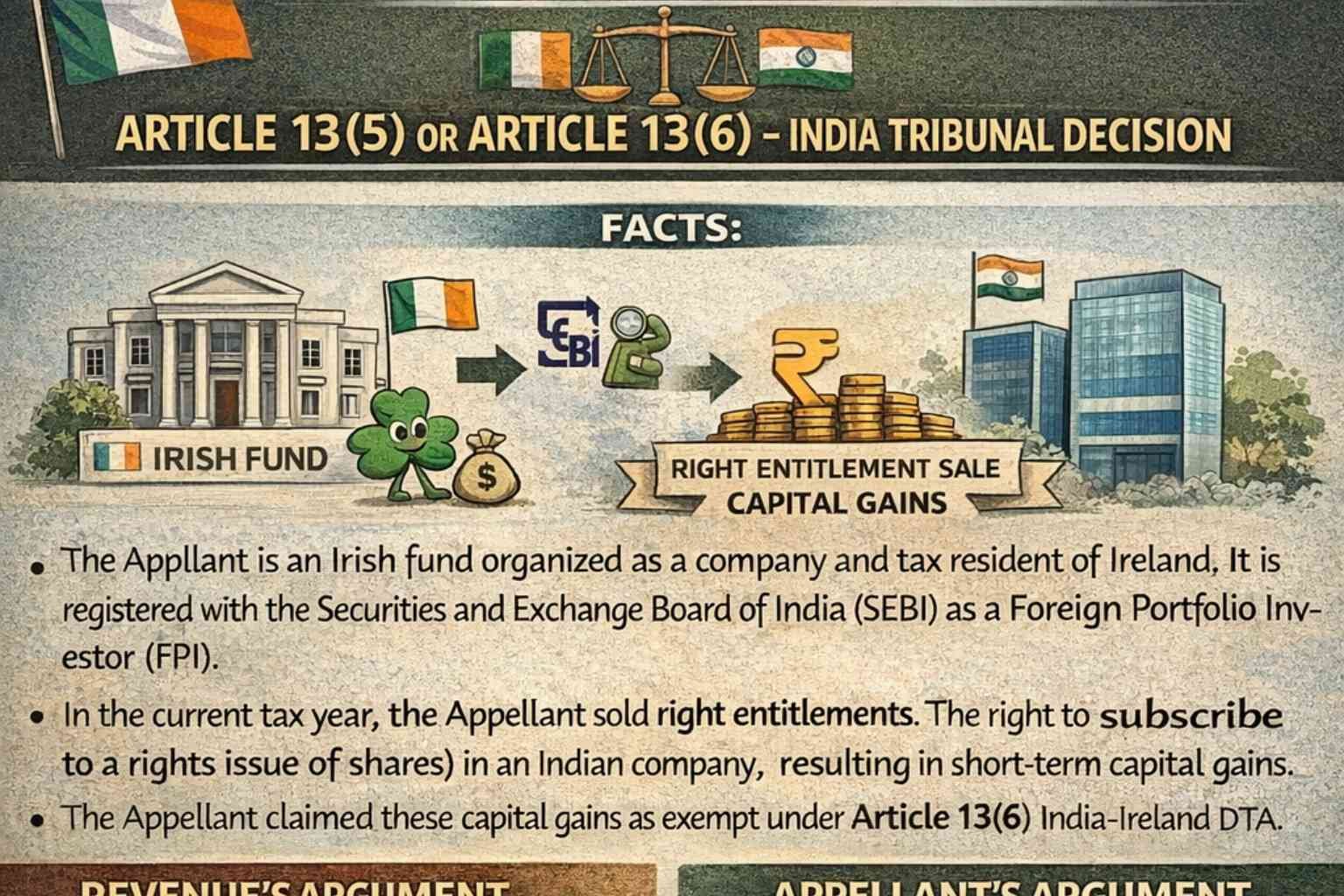

Article 13(5) or Article 13(6) – India Tribunal Decision

Facts: The Appellant is an Irish fund organized as a company and tax resident of Ireland. It is registered with the Securities and Exchange Board of India (SEBI) as a Foreign Portfolio Investor (FPI). In the current tax year, the Appellant sold right entitlements (the right to subscribe to a rights issue of shares) in an Indian company, resulting in short-term capital gains. The Appellant claimed these capital gains as exempt under Article 13(6) [residuary clause] of the India-Ireland Double Taxation Agreement (DTA).

Revenue’s Argument: The Revenue argued that Article 13(5), rather than Article 13(6), should apply, asserting that rights entitlements, due to their ability to be used to purchase shares at a discount, are akin to equity shares. They contended that shareholders’ eligibility to apply for the rights issue aligns more closely with shares, thus falling under Article 13(5). According to the Revenue, shares under this article should be interpreted broadly to include rights entitlements.

Appellant’s Argument: The Appellant maintained that there is a clear distinction between shares and rights entitlements under Indian Companies law, SEBI regulations, and income tax law. They also cited a Supreme Court decision ruling that rights entitlements are distinct from shares.

Tribunal Decision: The Tribunal accepted the Appellant’s argument and made the following observations:

- “Comparable interest” was included alongside “shares” in the Multilateral Instrument (MLI). However, post-MLI amendments did not include “comparable interest” in Article 13(5), indicating that Article 13(5) of the India-Ireland DTA refers solely to shares of a company and not other interests in shares.

- Rights entitlements were deemed similar to derivatives; therefore, the sale of rights entitlements would fall under the residuary clause, Article 13(6).

Based on the above, the Tribunal ruled that the capital gains from the sale of rights entitlements would be taxable only in Ireland under Article 13(6) of the India-Ireland DTA.

Interesting Fact: Under Irish corporation tax law, the computation mechanism for the sale of rights entitlements treats such rights as part of the share itself. Thus, the sale of such rights is considered a part-disposal of the original shareholding.