This content is for Subscriber members only.

UK Court decision

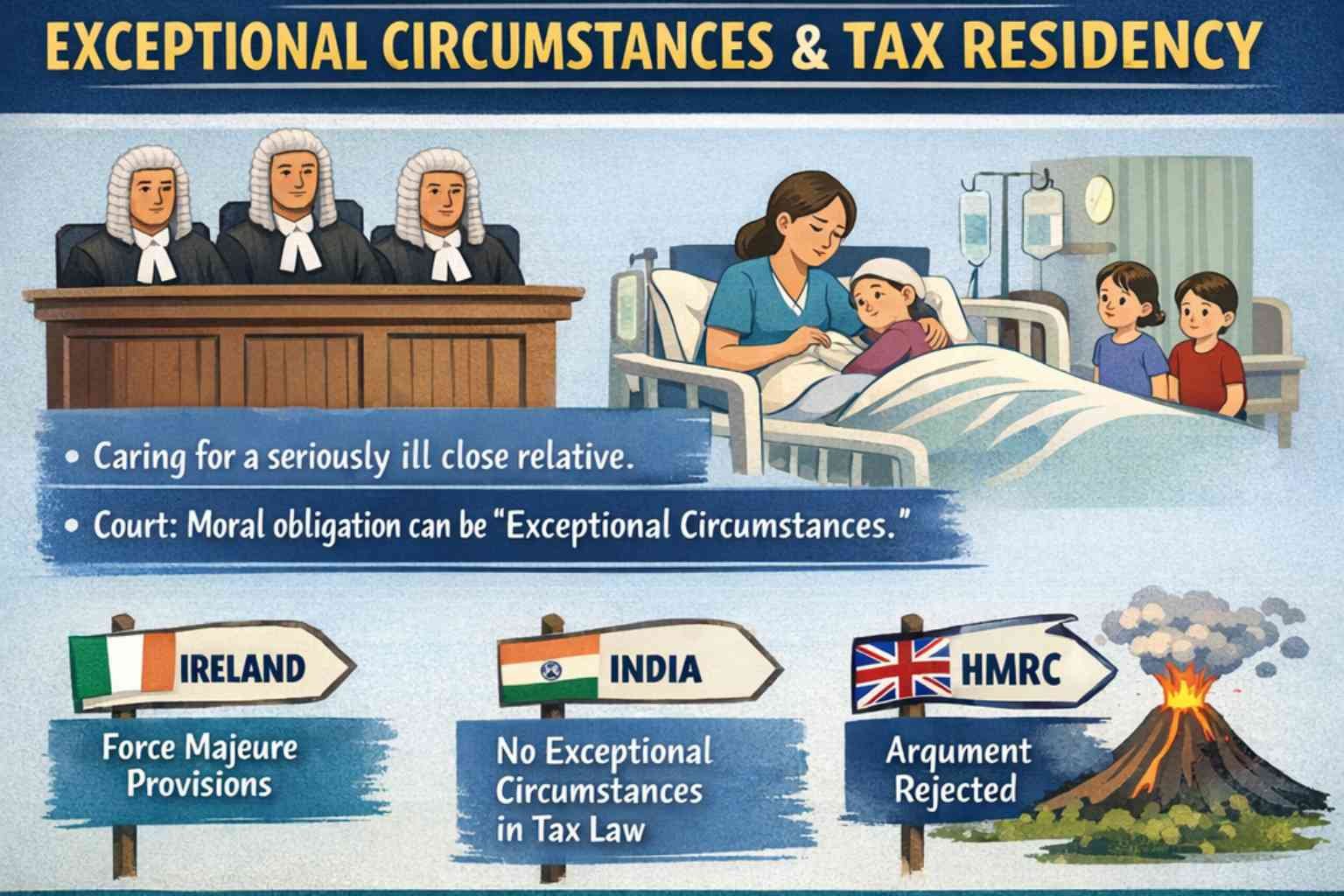

In the UK, income tax residency depends on the number of days an individual stays in the country and sufficient ties with the UK like family, accommodation, or work. A day won’t count if the individual stays due to “exceptional circumstances” beyond their control which prevents the individual from leaving UK and intends to leave as soon as those circumstances permit.

The UK Court of Appeal recently ruled that “exceptional circumstances” include moral or societal obligations to care for close relatives during severe illness. In this case, twin sister of the individual was ill and needed care including her minor children. These caregiving days (6 days in this case) were excluded from residency determination, resulting in the individual being non-resident in the UK.

The determination of exceptional circumstances as a point of fact or law was also discussed in detail by the court and ruled that it is a point of fact to be decided by the first-tier tribunal.

HMRC argued that exceptional circumstances should apply only with legal obligations to take care of the close relatives or physical prevention from leaving, like a volcanic eruption which made flights impossible etc. The court rejected this argument.

Ireland Income tax – revenue guidance includes force majeure circumstances, somewhat similar to UK Income tax provisions. It will be interesting to see if Irish courts consider this decision in appropriate cases.

India Income tax – income tax law does not address exceptional circumstances, nor does revenue guidance (except for covid-19 situations). Including these provisions in the new Income tax law could prevent significant tax impacts on individuals.

Domicile of an individual!!

In the United Kingdom, Ireland, and several other countries, income tax law incorporates the concept of domicile alongside tax residency to determine an individual’s income tax scope. Additionally, Article 4 of the model conventions refers to domicile for the purpose of establishing tax residency.

What precisely is an individual’s domicile?

This article provides a fundamental explanation of the domicile concept, which can be explored further through the link below.