This content is for Subscriber members only.

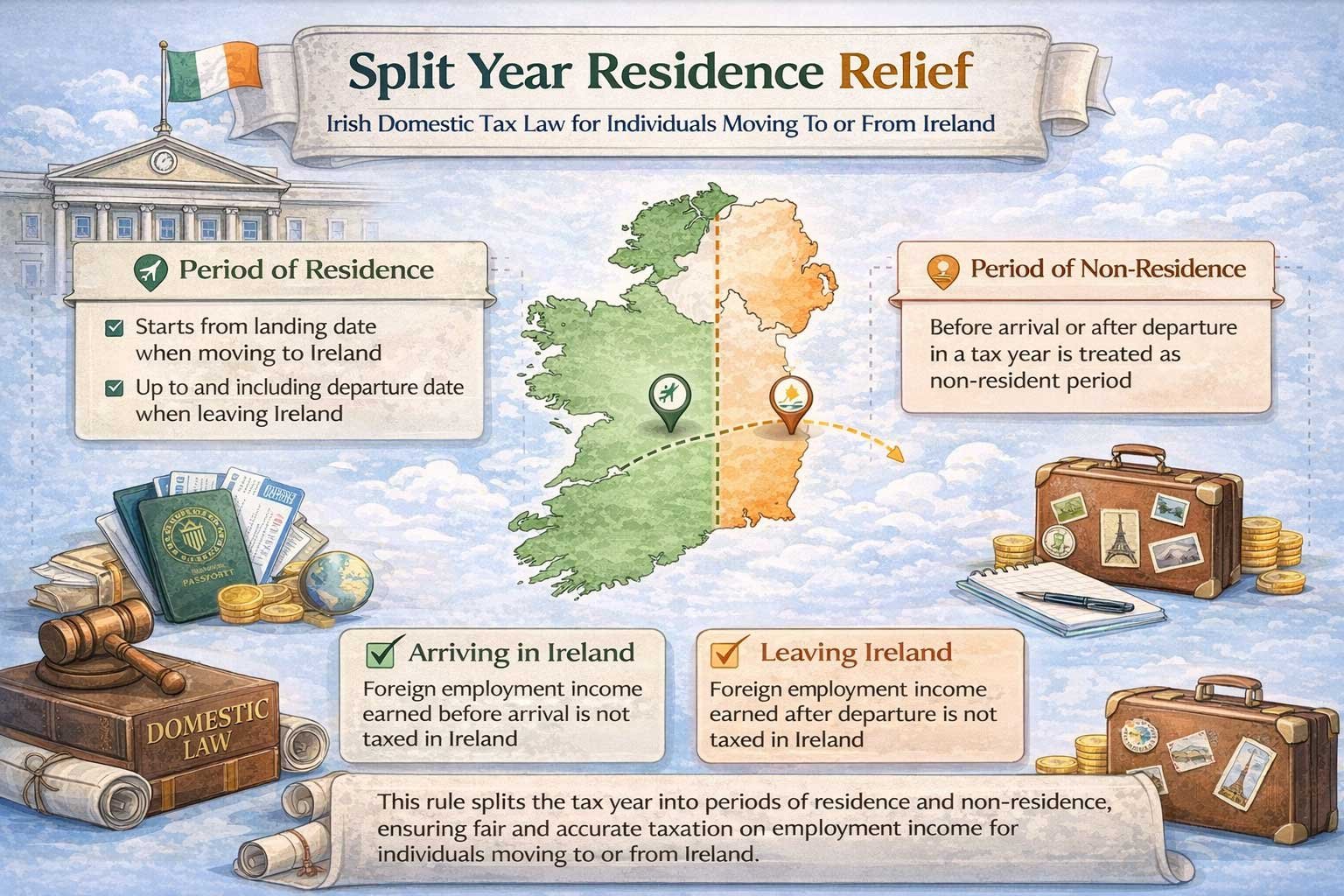

Split year residence relief

This rule in Irish domestic tax law is particularly relevant for individuals who move to or from Ireland during a tax year for employment. It allows for the tax year to be split into two parts – period of residence and period of non-residence. Once all the conditions are satisfied, the split year treatment affects the taxation of employment income as follows:

- Period of Residence: For those arriving in Ireland, it starts from the landing date. For those leaving Ireland, it is upto and including the departure date.

- Period of Non-Residence: The period other than the period mentioned above in a tax year.

- Individual arriving in Ireland: Foreign employment income earned before arriving in Ireland is not taxed in Ireland.

- Individual leaving Ireland: Foreign employment income earned after leaving Ireland is not taxed in Ireland.

This ensures that individuals are not unfairly taxed on income earned abroad when they are not residents of Ireland and prevents double taxation.

Administrative requirements: The individual must claim this relief in writing to the Revenue. However, an amendment in the Finance Act 2024 (apply from tax year 2026) allows the relief if all conditions are met, even without a claim by the taxpayer.

Important point: One of the conditions to apply this relief is that the individual must be resident in the current year of arrival or departure. The question is whether an individual can rely on the deemed residency rule in the current year even if the183/280 days rule is not satisfied? The answer is yes!

You can reach out to me in case of any queries on this.