This content is for Subscriber members only.

Interpreting the words “incidental to”

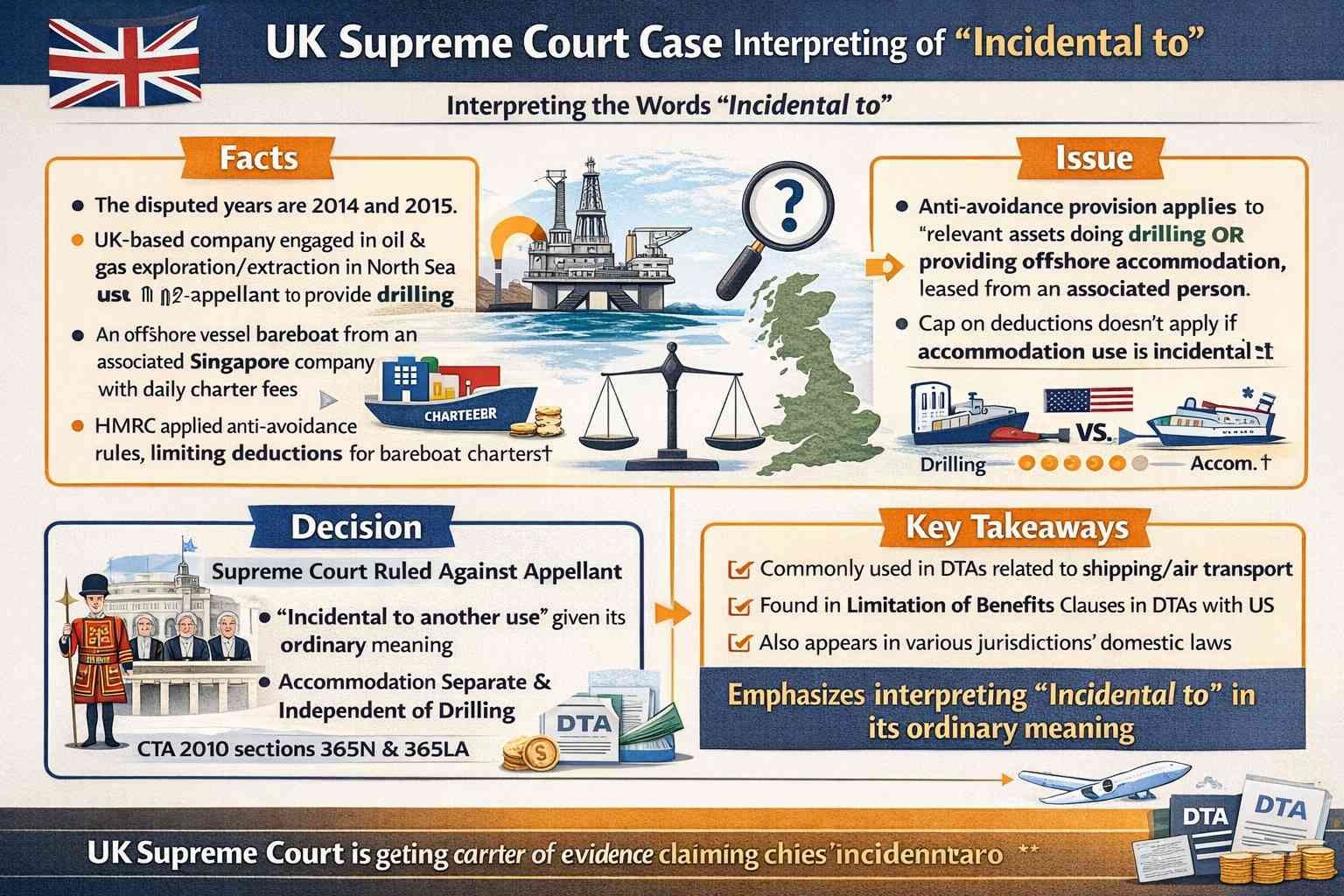

Facts:

The disputed years are 2014 and 2015. A UK-based company engaged in oil and gas exploration and extraction in the North Sea hired the appellant (UK resident corporation) to provide drilling services and accommodation for personnel using a specific vessel. This vessel was leased from an associated company based in Singapore on a bareboat charter basis, and the charter fee was paid daily. The charter fee was fully allowed as a deduction in the corporate tax return. However, Revenue applied anti-avoidance provisions under CTA 2010 sections 365N and 365LA, capping these deductions.

The UK Government aimed to prevent the oil and gas industry from using bareboat charters between connected parties to move significant taxable profit outside the UK. Part 8ZA of the CTA 2010 introduced a cap on lease payment deductions for drilling rigs and accommodation vessels leased between connected parties from 1 April 2014.

Issue:

The anti-avoidance provision applies when a relevant asset (in this case, a vessel) is used for drilling OR providing offshore worker accommodation and is leased from an associated person. The cap doesn’t apply if the accommodation use of the vessel is incidental to its primary use. The appellant’s vessel was used for both drilling and accommodation. The cap would not apply if it could be proved that providing accommodation was incidental to drilling services.

Decision:

The Supreme Court ruled against the appellant, accepting the Court of Appeal’s decision:

- “Incidental to another use” should be given its ordinary meaning.

- Accommodation services were not incidental to drilling services as they were separate and independent uses.

- The contract specifically included provisions for additional accommodation for personnel on the vessel, with separate charges agreed upon. This supports the point that accommodation was treated as a distinct and independent service.

Thus, the cap on charter fees applied since accommodation was not incidental to drilling.

Key takeaways:

The phrase “incidental to” is commonly used in Double Taxation Agreements (DTAs) related to shipping and air transport article, Limitation of Benefits clauses in DTAs with US, as well as in various jurisdictions’ domestic laws. This case emphasizes the importance of interpreting “incidental to” with its ordinary meaning.

#UKCorporateTax