This content is for Subscriber members only.

POEM interpretation – Article 13 read with Article 4 of UK-Mauritius DTA

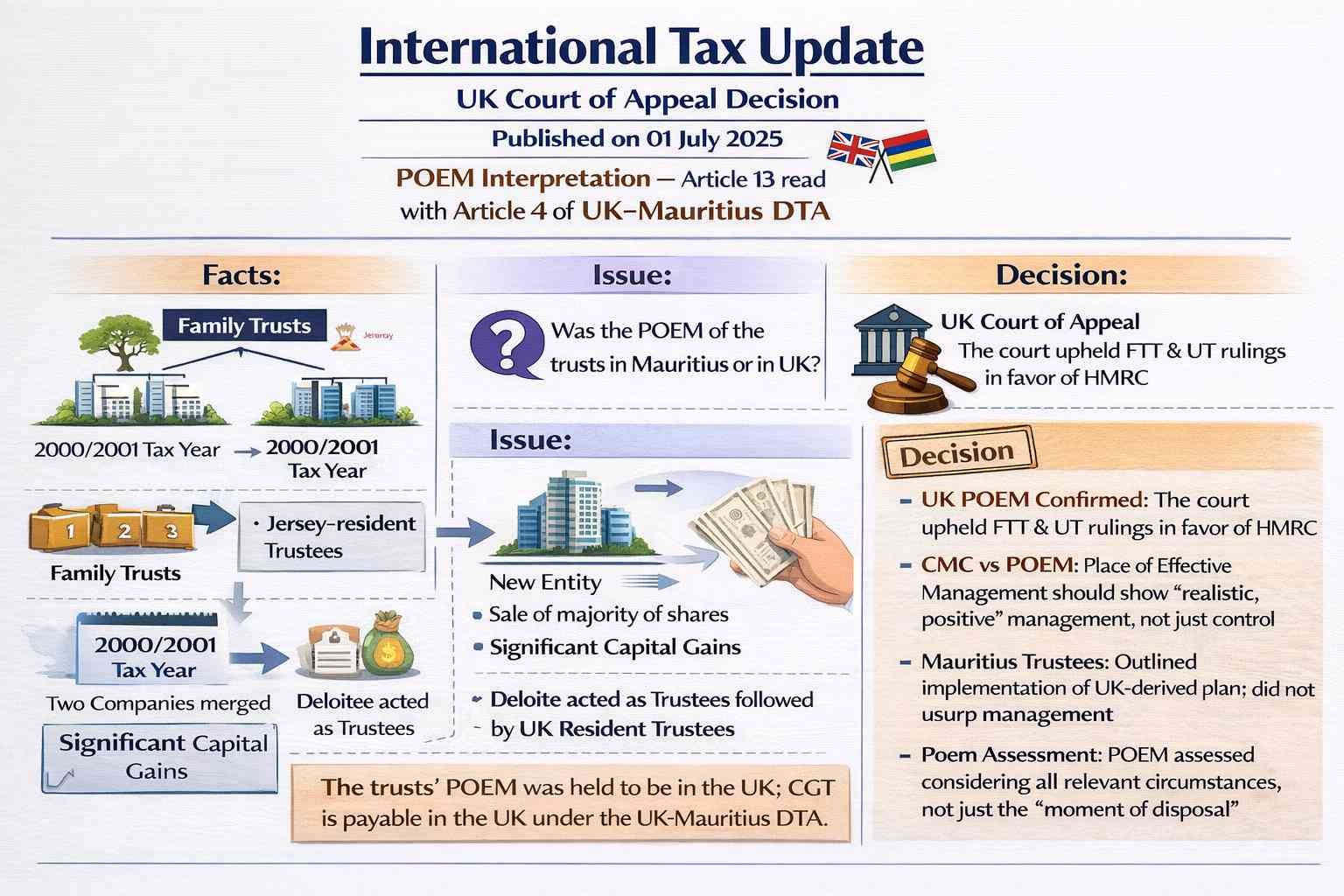

Facts:

Three family trusts (“the trusts”) were established in the United Kingdom, with trustees who were residents of Jersey. The disputed year is 2000/2001 tax year. The trusts held shares in two companies that subsequently merged to form a new entity, with the trusts holding all shares post-merger. During the disputed tax year, the settlors appointed Deloitte and one of its directors as trustees for part of the year, followed by UK residents as trustees for the remainder (as part of a strategy intended to avoid capital gains tax (CGT) under UK law). In the same period, the trusts sold a majority of their shares in the new company, resulting in significant capital gains. Neither the trusts nor the settlors paid CGT in the UK, relying on Article 13(4) in conjunction with Article 4(3) of the UK-Mauritius Double Tax Treaty.

The appellants contended that the place of effective management (POEM) for the trusts was Mauritius, arguing that central management and control (CMC) resided there. Accordingly, they asserted that, under Article 13(4), CGT should be taxable solely in Mauritius, which does not impose CGT domestically.

Issue:

Whether the POEM of the trusts was situated in Mauritius or in the UK. If in Mauritius, no CGT liability would arise in the UK; if in the UK, such liability would exist.

Decision:

The court found in favour of HM Revenue & Customs, upholding the decisions of both the First-tier Tribunal (FTT) and the Upper Tribunal (UT), making these key findings:

- CMC is distinct from POEM; while an entity may have multiple CMCs, it can possess only one POEM at any given time, intended as a tie-breaker.

- The appellant relied on Wood v Holden, where the court found that a company’s CMC resides where constitutional organs make decisions, barring usurpation by outsiders. However, the court distinguished POEM as requiring “realistic, positive” management, considering matters more broadly than CMC.

- The court determined that the overarching plan originated in the UK and that the role of the Mauritian trustees was predetermined. Although the Mauritian trustees fulfilled their duties and made genuine decisions, these decisions were in accordance with a plan devised by the settlors. Thus, even during the tenure of the Mauritian trustees, effective management resided elsewhere. The Mauritian trustees essentially executed instructions within a framework set by others, without acting improperly.

- POEM should be assessed with regard to all relevant circumstances, not merely those at the “moment of disposal.”

On this basis, the court concluded that the trusts’ POEM was located in the UK, rendering them resident in the UK for tax purposes. Consequently, CGT was found to be payable in the UK under the treaty.

#InternationalTax