This content is for Subscriber members only.

Capital nature of the dividends!!

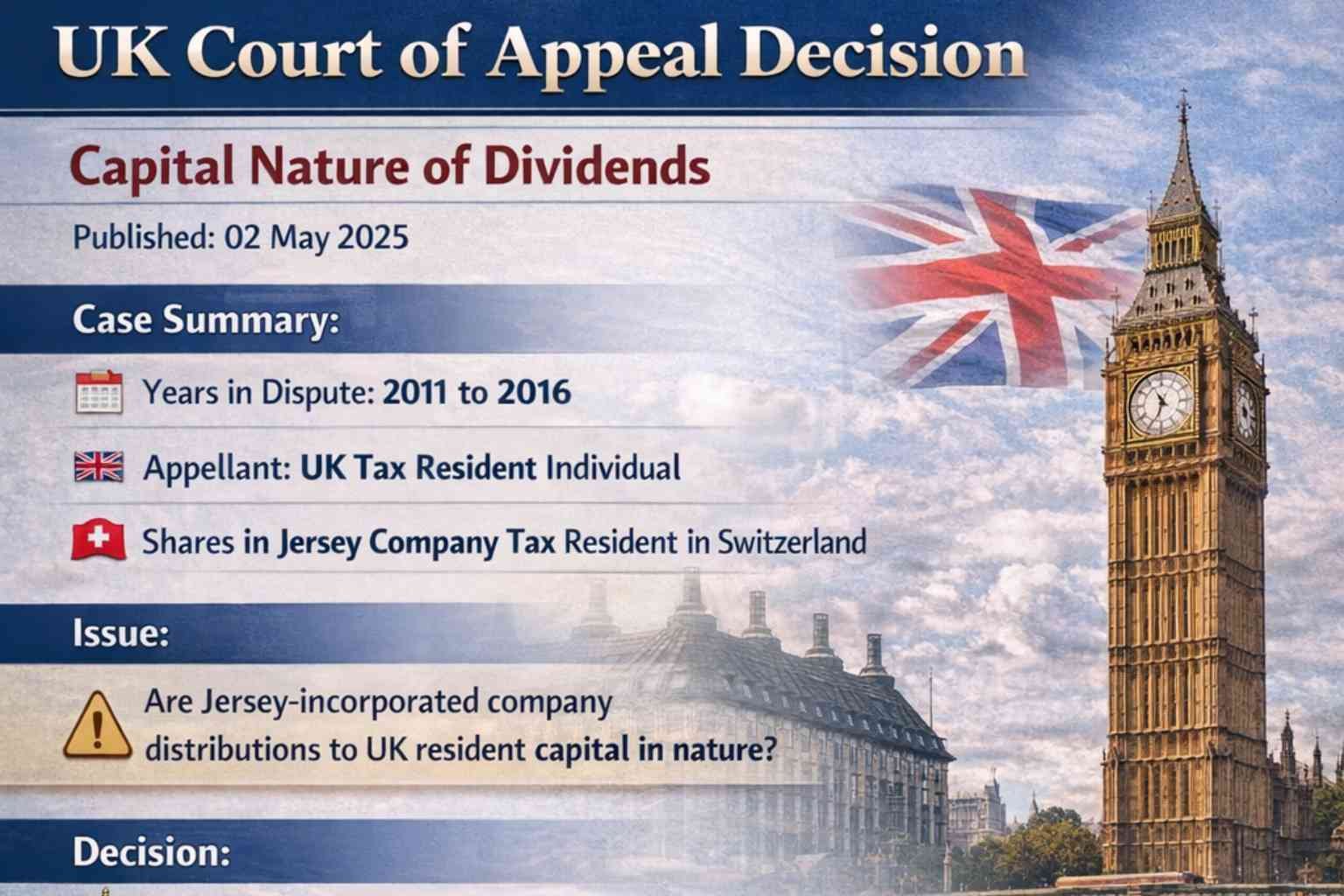

Facts:

The years in dispute are 2011 to 2016. The appellant is an individual and a tax resident of the UK. He owned ordinary shares in a company that is incorporated in Jersey and a tax resident in Switzerland. The dispute concerns distributions made by the company to shareholders, which were debited to the company’s share premium account as permitted under Jersey law. The appellant claimed that these distributions fall outside the charge to income tax because the dividends were of a capital nature under the UK income tax law. HMRC and the lower courts concluded that the distributions were dividends but were not of a capital nature and were thus taxable in the UK.

Issue:

The issue is whether the distributions made by the Jersey-incorporated company to the UK resident individual are of a capital nature. If so, they would not be taxable in the hands of the appellant under the UK income tax law.

Decision:

The court agreed with the lower courts and concluded that the distributions were not of a capital nature and accordingly taxed in the hands of the UK resident. The decision was based on the following points:

- The determinative test to establish whether a distribution is of a capital nature is the mechanism and form under which the distribution was made, rather than the source of funds from which the distributions were made.

- The test of whether the corpus of the asset remains intact after the distribution is not separate or different from the one focusing on the mechanism applied. Instead, the mechanism or form of the distribution is essential in determining whether the corpus, or capital, of the asset is regarded as left intact.

- The foreign system of law should be applied to determine the nature and characteristics of the transaction (distribution in this case). However, the proper interpretation and scope of the expressions “dividend” and “of a capital nature” are undoubtedly questions of UK law.

- Earlier case laws were relied upon to determine the character of the dividend.

Based on the above points, it was found that the mechanism used for the distribution by the Jersey company was under Part 17 of the Jersey Law, which allows the use of the share premium account for distributions similar to those made out of profits. Consequently, the distribution involved was not of a capital nature and was accordingly taxed in the hands of the appellant.

#UKTax, #InternationalTax