This content is for Subscriber members only.

Foreign jurisdiction’s domestic tax laws are critical in any tax planning!!

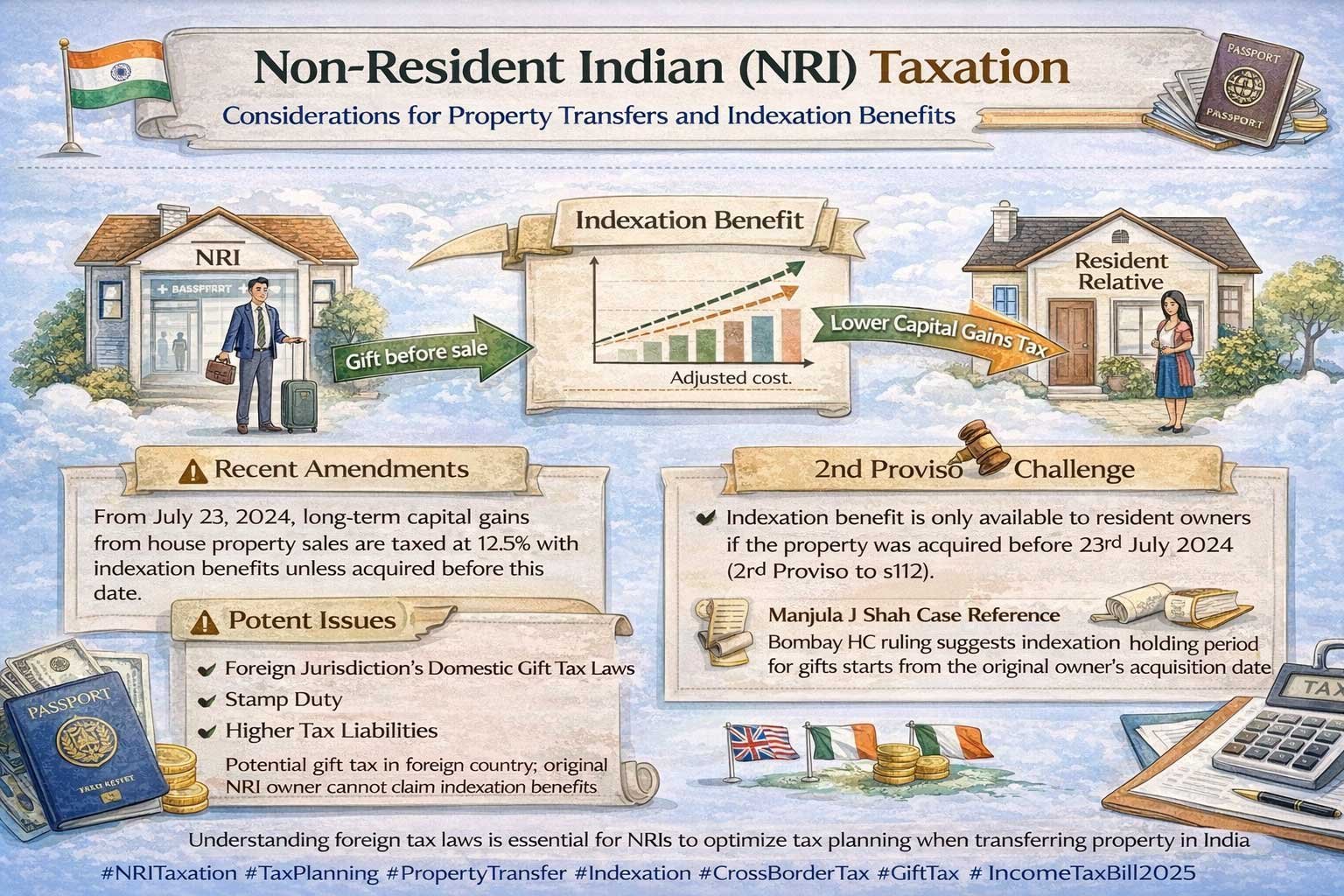

Navigating the intricacies of NRI taxation requires careful consideration, especially when transferring property in India. Based on some advice, an interesting scenario involves an NRI contemplating gifting their house property to a resident relative before it is sold. This strategy is suggested to utilize indexation benefits for computing capital gains.

According to recent amendments in Indian income tax law, the transfer of long-term capital assets is taxed at 12.5% without the indexation benefit. However, indexation relief is available if the house property was acquired before 23rd July 2024 and transferred thereafter. This allows the benefit of indexation through a specific calculation mechanism, but this relief is only available to resident transferors and not to non-residents (2nd Proviso to s112).

Even if the property is gifted to a resident relative, claiming the indexation relief presents challenges. The 2nd proviso states that the asset must be acquired before 23rd July 2024. Since the recipient of the gift would acquire the property post that date, the advice relies on the Manjula J Shah case from the Bombay High Court (355 ITR 474). This case suggested that, for gifts, the holding period for indexation purposes starts from the acquisition date of the original owner. So, if the NRI (the original owner) acquired the property before 23rd July 2024, this date should be considered for the recipient of the gift.

This approach has potential issues:

– The Bombay High Court’s decision may not be applicable in this context. In that case, the taxpayer was already eligible for the indexation benefit, whereas, in this situation, the eligibility itself is under question. Therefore, the resident recipient of the gift acquiring the property after 23rd July 2024 may not be entitled to indexation (under the 2nd proviso to s112).

– Stamp duty will be applicable for the registration of the gift deed in India.

– The country of residence of the NRI might levy a gift tax (as seen in the UK/Ireland), depending on the residency and domicile of the donor. For instance, Ireland has a distinct gift tax law that may be applicable in this scenario. Furthermore, the donor might be subjected to capital gains tax in their country of residence. Threshold limits for exemption, Relief or credit in the foreign jurisdiction must be analyzed based on the specific facts and circumstances, as gift tax is not covered by the Double Taxation Avoidance Agreement (DTAA) between India and Ireland/UK.

This could result in higher tax liabilities compared to a direct transfer by the NRI. Therefore, it is imperative to consider the domestic laws of the foreign jurisdiction when engaging in cross-border tax planning.

Separately, I was hoping for the relief of indexation to be extended to the NRI in the new Income tax Bill 2025 which is not the case.

NRITaxation #TaxPlanning #PropertyTransfer #Indexation #CrossBorderTax, #gifttax #Incometaxbill2025