This content is for Subscriber members only.

What about foreign losses?

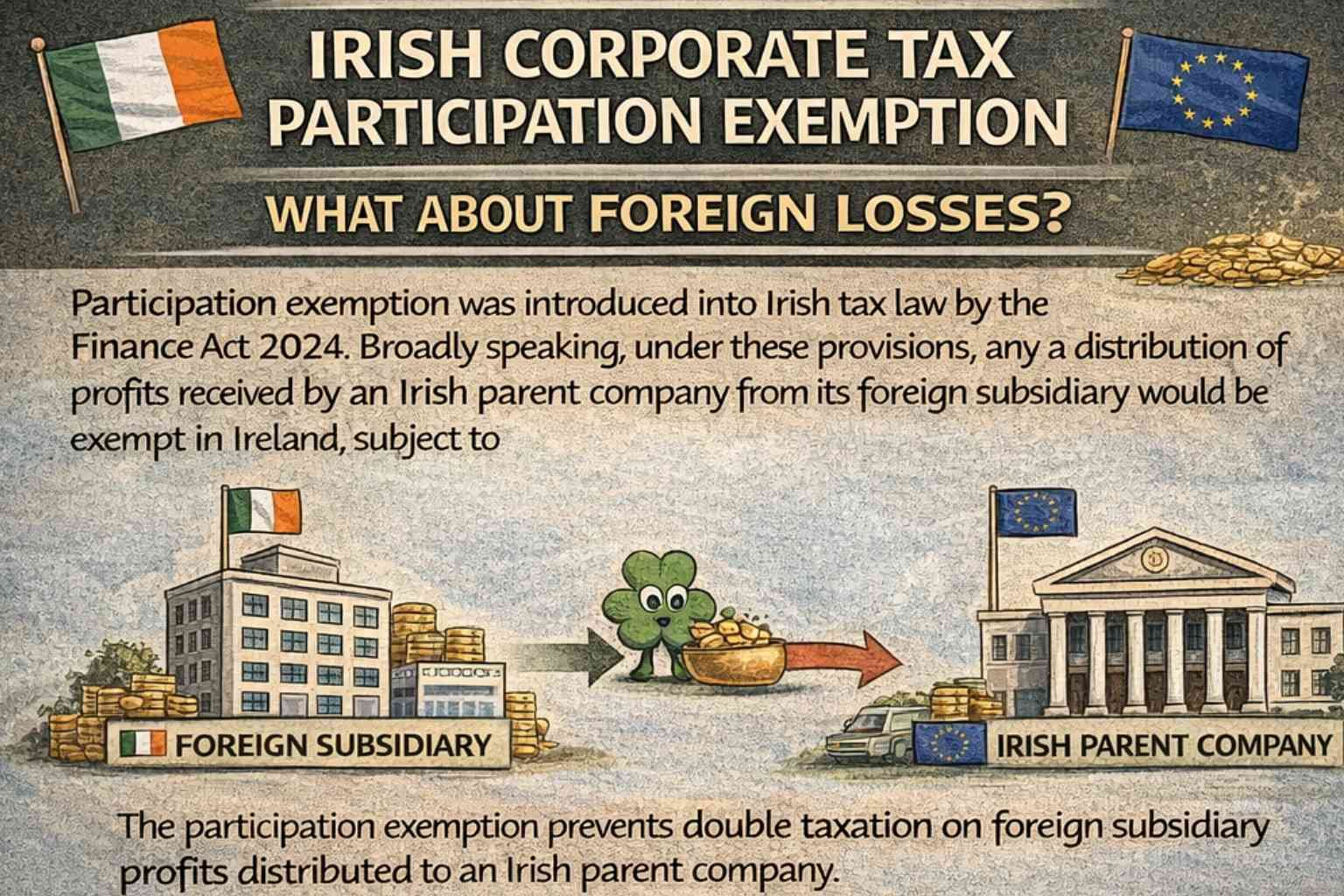

The participation exemption was introduced into Irish tax law by the Finance Act 2024. Broadly speaking, under these provisions, any distribution of profits received by an Irish parent company from its foreign subsidiary would be exempt in Ireland, subject to certain conditions being met.

The purpose of the participation exemption is to prevent double taxation on the profit of the subsidiary, which is already taxed (corporate tax) in the foreign jurisdiction, as well as on the distribution of such profits.

However, there are two questions that arise which, in my view, are not addressed by the current provisions of the participation exemption and require clarification:

- Whether the losses of the foreign subsidiary (resident in an EU member state/EEA) would be allowed to be transferred to the Irish parent under section 420C (if all conditions are satisfied), despite the participation exemption applying to profit distribution from the same subsidiary?

- How would the liquidation loss be treated following the liquidation of the foreign subsidiary? Specifically, whether such loss would be allowed to be set off against the income of the Irish parent company in the year of completion of liquidation? In layman’s terms, the liquidation loss is the original investment amount by the parent company that exceeds the liquidation proceeds.

There are two potential approaches to addressing these situations:

- Allowing the foreign subsidiary’s losses to be set off against the income of the Irish parent under section 420C (if all conditions satisfied) in the earlier years (than the year of liquidation of subsidiary). In this case, the same amount of losses set off earlier should be adjusted when calculating the liquidation loss upon completion of liquidation. The remaining liquidation loss should then be allowed to be set off against the income of the Irish parent company if all the conditions under s420C is satisfied.

Note: The UAE corporate tax law adopts this approach; however, this mechanism is applicable to two or more UAE-resident companies.

- Disallowing the foreign subsidiary’s losses to be set off against the income of the Irish parent in the earlier years. Consequently, the total amount of the liquidation loss should be allowed to be set off against the income of the Irish parent company in the year of completion of liquidation if all the conditions under s420C is satisfied.

It would be beneficial if Revenue provided necessary amendments and guidance on these matters for the sake of completeness and clarity.

Vidarbha Veneere Industries Ltd. Versus Income Tax Officer Ward-7 (1), Nagpur. Bombay High Court

This will not end here…….

This issue will not be resolved until necessary amendments are made to the income tax law.

The Transfer of Property Law in India says that land includes interests in land, and creating or assigning leasehold rights counts as a transfer. Makes sense, right? Of course, the Revenue wants to tax these transfers as capital gains tax on this basis.

But the current income tax law and its strict interpretation don’t allow it. Section 50C talks about “capital assets being land or building or both” and leaves out any interests in them.

Another big issue is figuring out capital gains. Leasehold rights are part of the land being transferred, but there’s no clear way to determine the cost of acquisition for the leasehold right. The law doesn’t give a method to split the cost between different rights in the land. I am surprised this ground was not raised but I am sure someone will.

Plus, things get messy when upfront premiums are paid along with monthly rents for the lease. Should these premiums be considered all capital, partly income and partly capital? And how do you calculate capital gain when there’s a sub-lease shorter than the head lease? Unless the law specifically addresses these issues, it doesn’t look like we’ll see a resolution anytime soon.