This content is for Subscriber members only.

Surcharge on late filing of iXBRL accounts

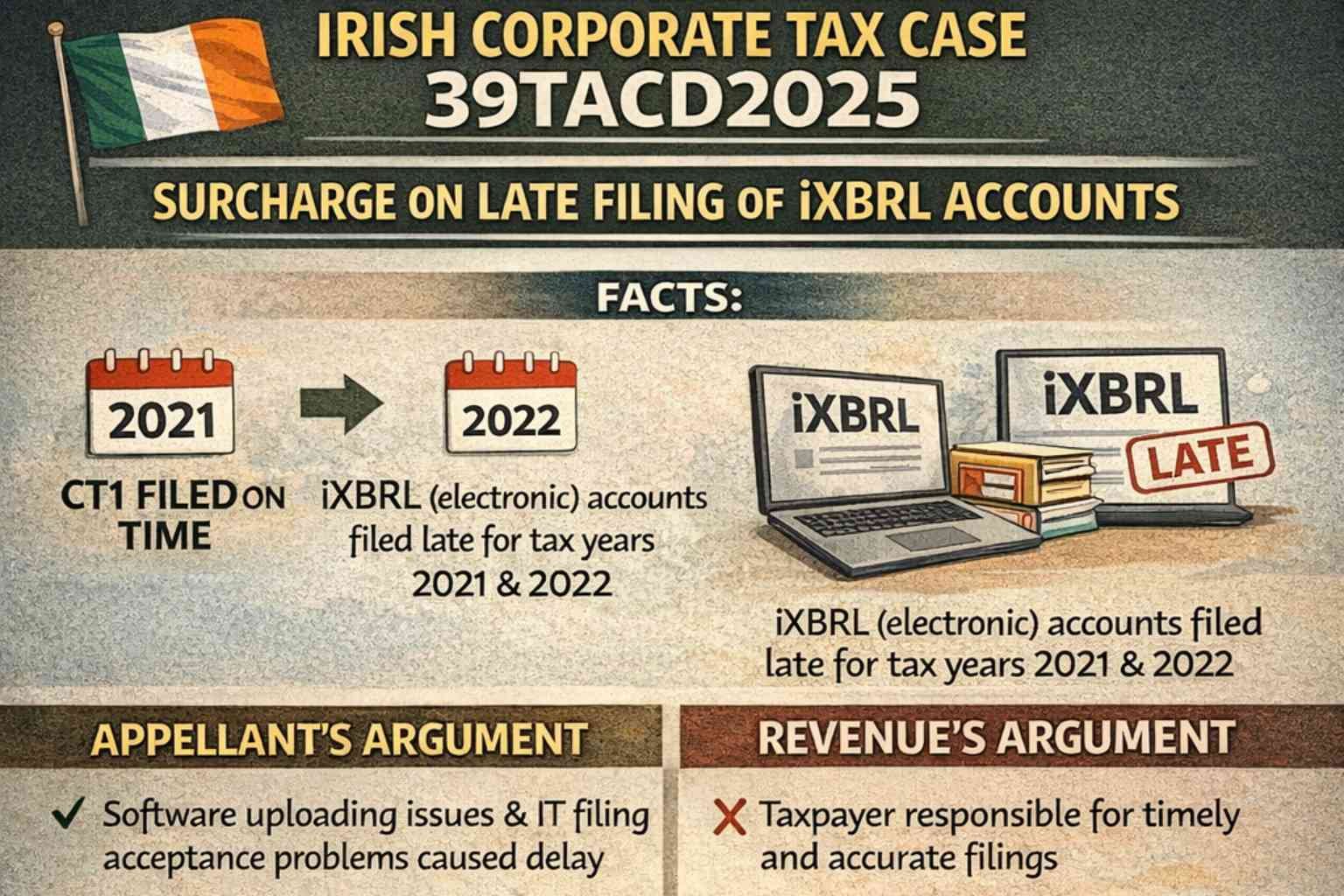

Facts: The appellant filed CT1 for the tax years 2021 and 2022 on time. However, the appellant submitted accounts in iXBRL format for both years beyond the filing deadline (i.e., after the grace period of 3 months).

Appellant’s argument: The appellant recalled experiencing software uploading issues and IT filing acceptance problems for the iXBRL accounts in both years. The appellant asserted that the non-filing of electronic statements was not intentional or deliberate and that it only became aware of the issue with the filing of electronic accounts in 2024 when the Revenue communicated about it. The appellant also argued that it was Revenue’s failure to alert them to the fact that iXBRL accounts had not been filed while continuing to issue tax clearance certificates. Additionally, the appellant claimed that Revenue’s software should automatically flag any filing failures.

Revenue’s argument: Revenue contended that it is not its responsibility to alert taxpayers about any failure to file returns. It emphasized that it is the taxpayer’s responsibility to correctly file all the returns. Revenue also noted that the appellant failed to communicate with them regarding the technical difficulties experienced in filing the accounts.

Decision: The Commissioner highlighted two important points in the ruling:

- This case does not involve a deemed delay in filing the return beyond the specified time limit [s1084(1)(b)(ii)]; rather, it involves an actual delay in filing the return, as the iXBRL accounts were not filed before the specified deadline.

- Even if the case were treated as a deemed delay in filing the return under section 1084(1)(b)(ii), the Commissioner found no basis to conclude that the error in the return was remedied without unreasonable delay. The appellant did not present evidence of contemporaneous correspondence to the respondent regarding technical difficulties with filing the accounts for both years. Therefore, the Commissioner does not view this as a case where the return can be said to have been remedied without unreasonable delay.

Accordingly, the Commissioner decided that the levy of the surcharge was proper and correct.

Key takeaways: While there may be genuine situations of inadvertent errors in the filed returns and iXBRL accounts, it is imperative to review the filed returns thoroughly. In the event of any errors, they should be remedied as soon as possible. Remedying those errors only after communication from the Revenue could be treated as not remedying those errors without unreasonable delay.