This content is for Subscriber members only.

Can foreign PE be considered as employer under the treaty?

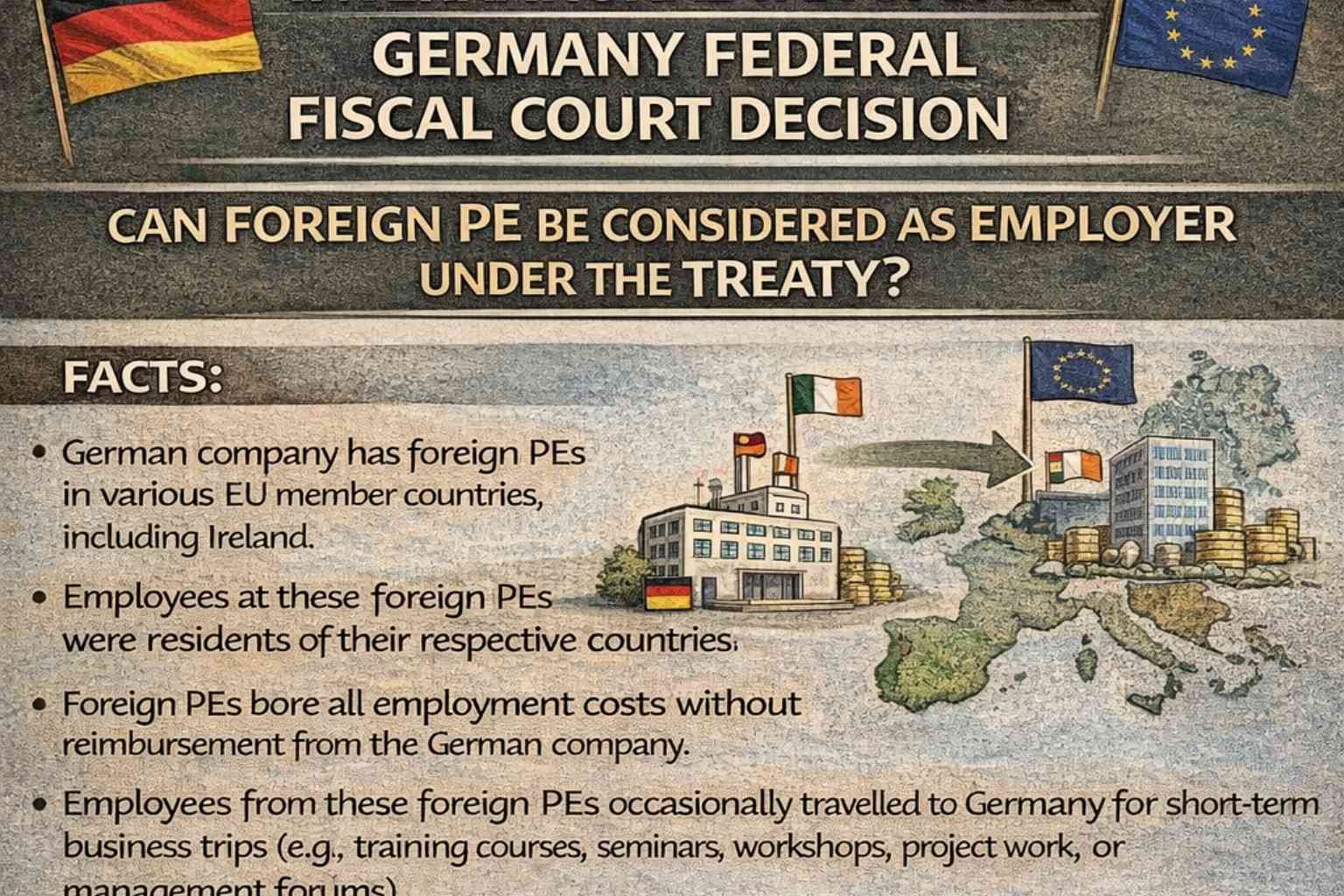

Facts: A company incorporated in Germany maintained foreign permanent establishments (PE) across various European Union member countries, including Ireland. Employees at these PEs were resident in their respective countries and were employed by the German company under its civil law framework. The foreign PEs incurred all employment costs without reimbursement from the German company.

Employees from these foreign PEs occasionally travelled to Germany for short-term business trips (e.g., training courses, seminars, workshops, project work, or management forums), which served the interests of their respective PEs.

Issue: The issue at hand is whether Article 14(2)(b) [equivalent to OECD model Article 15(2)(b)] of the Treaty with various European member countries can be satisfied by treating the foreign PEs as employers. Based on the facts provided, the conditions under Articles 15(2)(a) and 15(2)(c) of the OECD appear to be met. Should Article 14(2)(b) not be satisfied, the German company would be obligated to withhold tax on the portion of remuneration attributable to the business visits in Germany.

Decision: The court determined that foreign PEs of a legally independent person resident in Germany cannot be considered employers within the meaning of Article 14(2)(b), based on the following points:

- The court referred to Article 31 of the Vienna Convention and Article 3 of the treaties with various countries, noting that the term “employer” is not explicitly defined in the treaty. Thus, the treaty context must be considered first, followed by the domestic law meaning. The court cited an earlier Federal Fiscal Court decision, indicating that an employer within the meaning of treaty law could be not only the civil law employer but also another natural or legal person who economically bears the remuneration for the employment performed (economic employer). However, the court ruled that foreign PEs are not legal persons within the meaning of Article 3(1)(d) (definition of persons).

- The foreign branches are merely PEs of the appellant within the context of Article 5. Under treaty law, only a person who has the capacity to be a resident in one of the two contracting states within the relevant agreement can be considered an employer. Since a PE cannot be a resident, a domestic PE of a person resident abroad cannot be an employer.

- The wording of Article 15 in the OECD model precludes equating the term “employer” under treaty law with “permanent establishment”.

- The court held that the German company was both the employer under civil law and the economic employer. There is no other entity, besides the appellant, that economically bears the wages of the foreign workers.

- No provisions of the treaty regarding the functioning of the European Union were violated.

Key consideration: Employees working in Irish branches under similar circumstances should carefully evaluate claiming the foreign tax credit on the withheld tax income when filing their tax returns in Ireland.