This content is for Subscriber members only.

Word “business” interpretation under Article 18– Article 16 and 18 of Germany-Luxembourg DTA

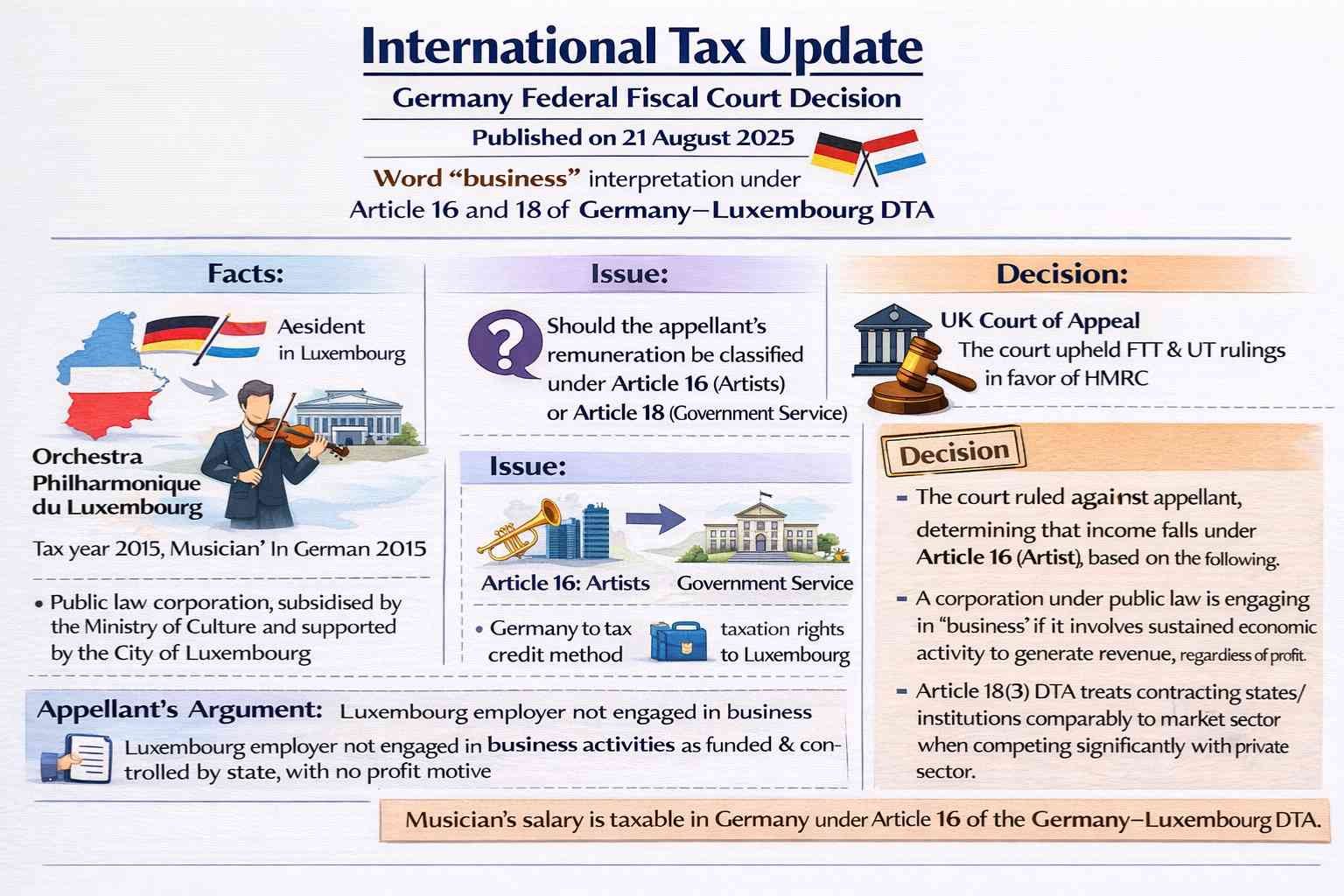

Facts:

The appellant, a resident of Germany in the tax year 2015, was employed as a musician (artist) by the Orchestre Philharmonique du Luxembourg. His employer is a public law corporation, subsidised by the Ministry of Culture of the Grand Duchy and supported by the City of Luxembourg. This entity qualifies as an organisation under Article 18 of the DTA (Government Service). The organisation actively promotes cultural reputation and organises cultural orchestra events and paid concerts pursuant to its state mandate, and it is not operated for profit.

Issue:

The primary issue concerns whether the appellant’s remuneration should be classified under Article 16 (Artists) or Article 18 (Government Service) of the DTA. Classification under Article 16 would grant Germany the right to tax the income, applying the credit method. Conversely, classification under Article 18 would allocate taxation rights exclusively to Luxembourg. Notably, Article 18(3) of the DTA specifies that Article 14 (Salary), Article 16 (Artists), and Article 17 (Pensions) may apply if the individual’s services are connected with business activities conducted by the state, a local authority or public law corporation like the employer in this case.

Appellant’s Argument:

The appellant contended that the employer organisation is not engaged in business activities in Luxembourg, as it operates under state control, is state-funded, and does not pursue profit-generating activities.

Decision:

The court ruled against the appellant, determining that the income falls under Article 16 (Artist), based on the following observations:

- A corporation under public law is considered to conduct business if it participates in sustained economic activity with the objective of generating revenue, regardless of profit motive.

- Article 18(3) of the DTA establishes that contracting states and their institutions are to be treated comparably to other market participants when they compete significantly with private sector entities.

- Neither Article 5 nor Article 7 requires that business activities be performed with intent to realise profits.

- Article 16 applies not only to self-employed individuals but also to those in employment relationships.

- Where the conditions of Article 16 are satisfied, it takes precedence over Article 14.

#InternationalTax