This content is for Subscriber members only.

30% rule on employment income – Article 14 and 22 of Germany-Netherlands DTA

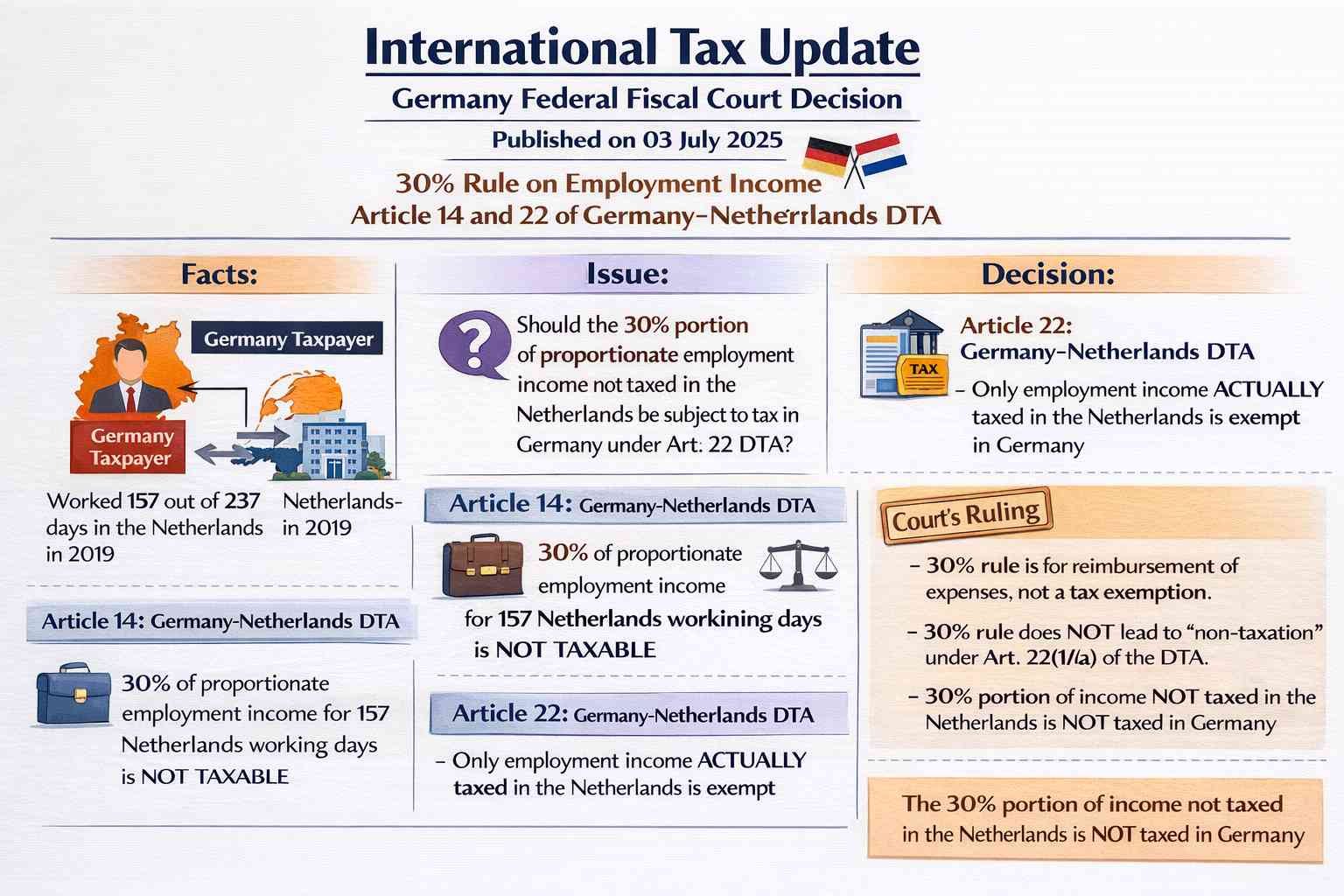

Facts:

The taxpayer is an individual tax resident in Germany and employed by a Netherlands-based employer. In the year 2019 (the relevant tax year), the taxpayer worked in the Netherlands for 157 out of a total of 237 working days.

Under Article 14 of the Germany-Netherlands Double Taxation Agreement (DTA), employment income corresponding to the number of days worked in the Netherlands is taxable there. According to the Netherlands’ tax law, 30% of this proportionate employment income (for 157 days) is not taxed in the Netherlands (so called “30% rule”).

Article 22 of the DTA stipulates that, to avoid double taxation, only the portion of employment income actually taxed in the Netherlands should be exempted from taxation in Germany (exemption method). The German tax authorities included the 30% portion of employment income, arguing it was not actually taxed in the Netherlands and therefore did not meet Article 22 requirements.

Note: Under the Dutch wage tax act, employees with Dutch employers who either relocate to the Netherlands for work or commute daily may receive reimbursement for additional expenses such as family travel, higher living costs, or visa/residency-related expenses. Employers can reimburse documented actual costs (with proof) or, alternatively, pay a flat rate equal to 30% of Dutch salary. In this case, the taxpayer’s employer applied the flat 30% rule.

Decision:

The court determined the following:

- The 30% rule constitutes lump-sum reimbursement for expenses rather than a personal or material tax exemption resulting in non-taxation. As such, it does not qualify as non-taxation under Article 22(1)(a) of the DTA.

- The 30% rule is a cost-related exemption rather than an exemption of income, even though its structure differs from reimbursements based on documented expenses.

As a result, the court held that the 30% portion of proportionate employment income not taxed in the Netherlands should not be included in the tax base in Germany.

#InternationalTax