This content is for Subscriber members only.

Fixed place PE – Germany-UK DTA

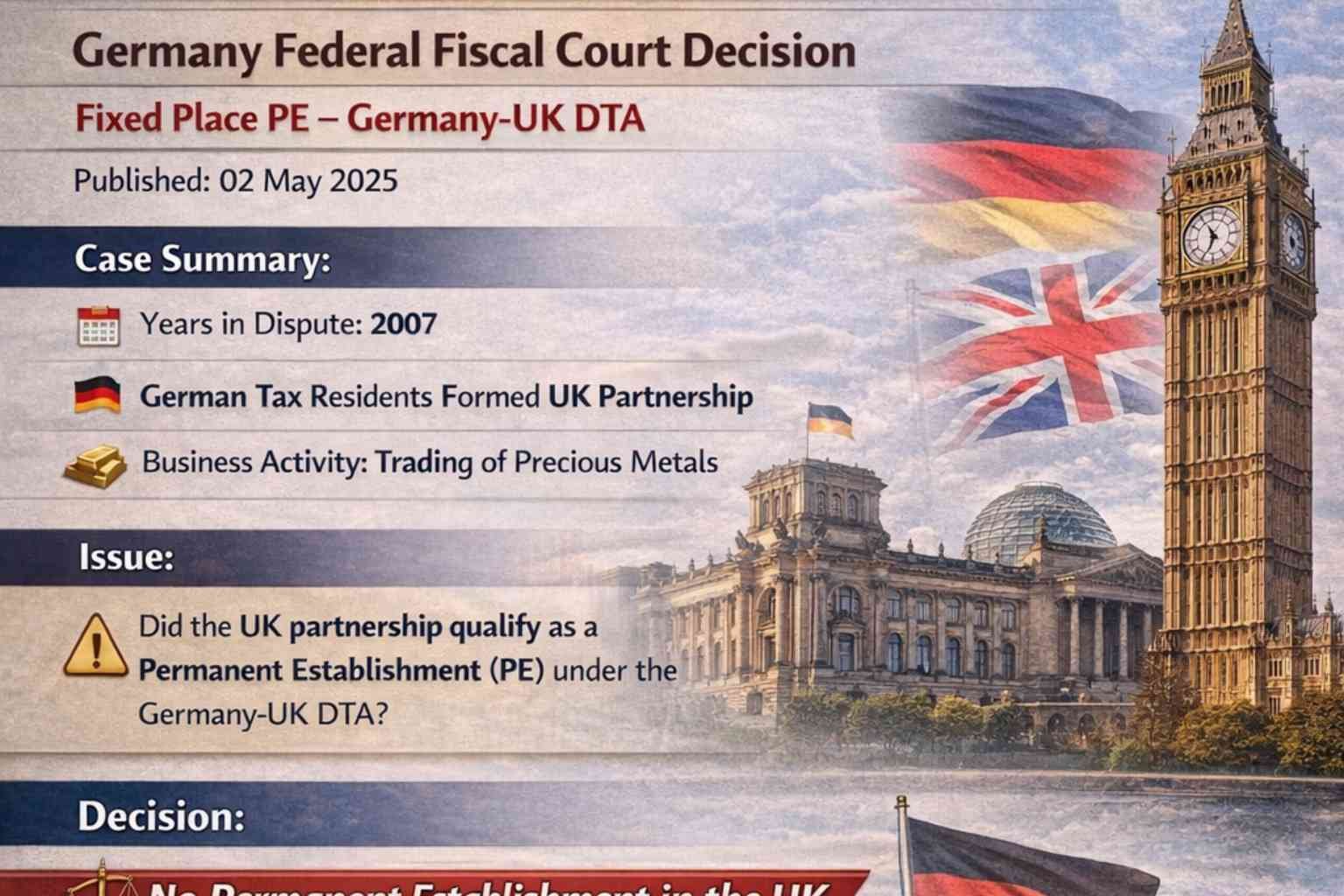

Facts:

The appellants were tax residents of Germany and formed a general partnership in the UK in September 2007. This partnership was engaged in the trading of precious metals. The year in dispute was 2007.

Issue:

Whether the partnership in the UK could be considered a permanent establishment (PE) under the Germany-UK Double Taxation Agreement (DTA). If so, the profits of the PE would be exempt from taxation in Germany under domestic law.

Decision:

The Court ruled that there was no PE in the UK and established two significant principles:

- A “fixed” business establishment requires a minimum duration of six months of existence in the foreign jurisdiction. This minimum period applies not only to the business facility but also to the business activity conducted within it. The period does not meet the requirement if extended only by the liquidation of a company.

- The existence of an undertaking for less than six months, even if conducted entirely within the business premises of the state where it is established, does not justify an exception to the minimum duration.

In this case, the period under consideration was from September 2007 to April 2008. The fact-finding authority (lower court) concluded that the core business activity of the partnership ceased in January 2008. The appellant argued that other business activities continued for more than six months, even after January 2008, and that the lease agreement remained active until April 2008.

The court rejected the appellants’ arguments, stating that merely continuing the lease agreement and ancillary activities did not satisfy the minimum duration requirement. It is the core business activities that must continue for at least six months.

Key takeaways:

This case brings to mind the Formula One decision of the Supreme Court of India, where the business activity continued for much less than six months but still triggered the PE in India. Furthermore, the OECD commentary on Article 5, paragraph 30, provides an exception for the minimum duration. Interestingly, Germany has reserved its position on this paragraph, as stated in paragraph 179, maintaining that a minimum duration of six months is necessary to trigger the PE.

#InternationalTax