This content is for Subscriber members only.

“Dependent personal services” article of Germany-France DTA

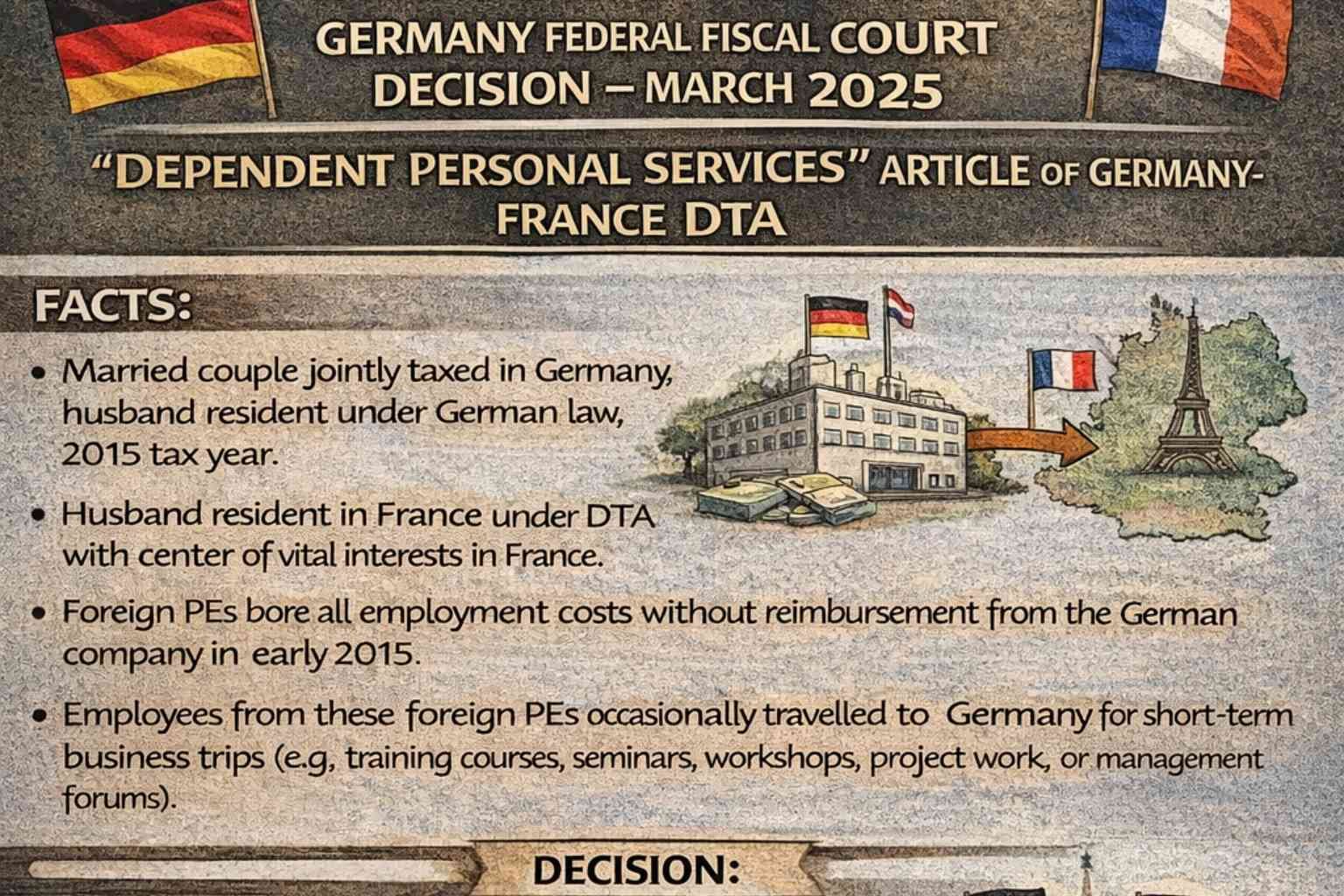

Facts: The appellants are a married couple who were jointly taxed in Germany. The appellant was resident in Germany under domestic law and taxable on his worldwide income for 2015, which is the year in dispute. The appellant was also resident in France under the DTA, and his central vital interest was in France.

From 2012 to 2014, the appellant was employed by a German company and performed his duties partially in Germany, France, and other third countries. The employment ended in early 2015. After his period of service, he received severance payments and was entitled to exercise ESOPs along with share allocations (non-cash benefits).

In their return of income in Germany, the appellant considered the severance payments and non-cash benefits to be completely or partially tax-exempt in Germany because they accrued after the end of the period of service. Appellant also submitted the tax paid in France for the severance payments and non-cash benefits. German tax authorities ultimately taxed the severance payments and non-cash benefits proportionate to the number of days of duties performed in Germany.

Decision: The Federal Court agreed with the lower courts’ decision. The Court laid down the following critical points:

- Severance payments and non-cash benefits form part of employment income, even if the employment has ceased, and therefore fall under the “Dependent personal services” article of the DTA.

- According to Article 13(1) of the DTA, income from employment may only be taxed in the state where the personal activity from which the income originates is carried out. Therefore, the court ruled that severance payments and non-cash benefits are required to be taxed to the extent of activities performed in Germany (for non-cash benefit – from the granting of the stock options or the promise of the future share allotments until the time of the first exercisability of the stock options or the share allocations).

- The Court mentioned that any double taxation in this case could be eliminated by filing an application under the mutual agreement procedure by the appellant.

The following questions need to be addressed to determine the taxability of ESOPs:

- How would accrual and receipt basis of taxation impact ESOP taxability?

- Is ESOP taxed in the year of grant, in the year of exercisability, or in the year of actual exercise?

- How do the terms and conditions of the ESOP affect its taxability?

- What happens if the ESOP’s exercisability or actual exercise occurs after the cessation of employment?

- In the international tax context, when should the residency of the employee be checked: on the date of exercise or in the past years when the income was accrued?

- How does the tax credit work in the case of different time of taxation rules under the domestic laws of two different states?

- In the international tax context, how is the income apportioned to multiple states?

I will write a detailed article on this topic in the Indian context and also varying rules in other jurisdictions.

Stay tuned!