This content is for Subscriber members only.

Background

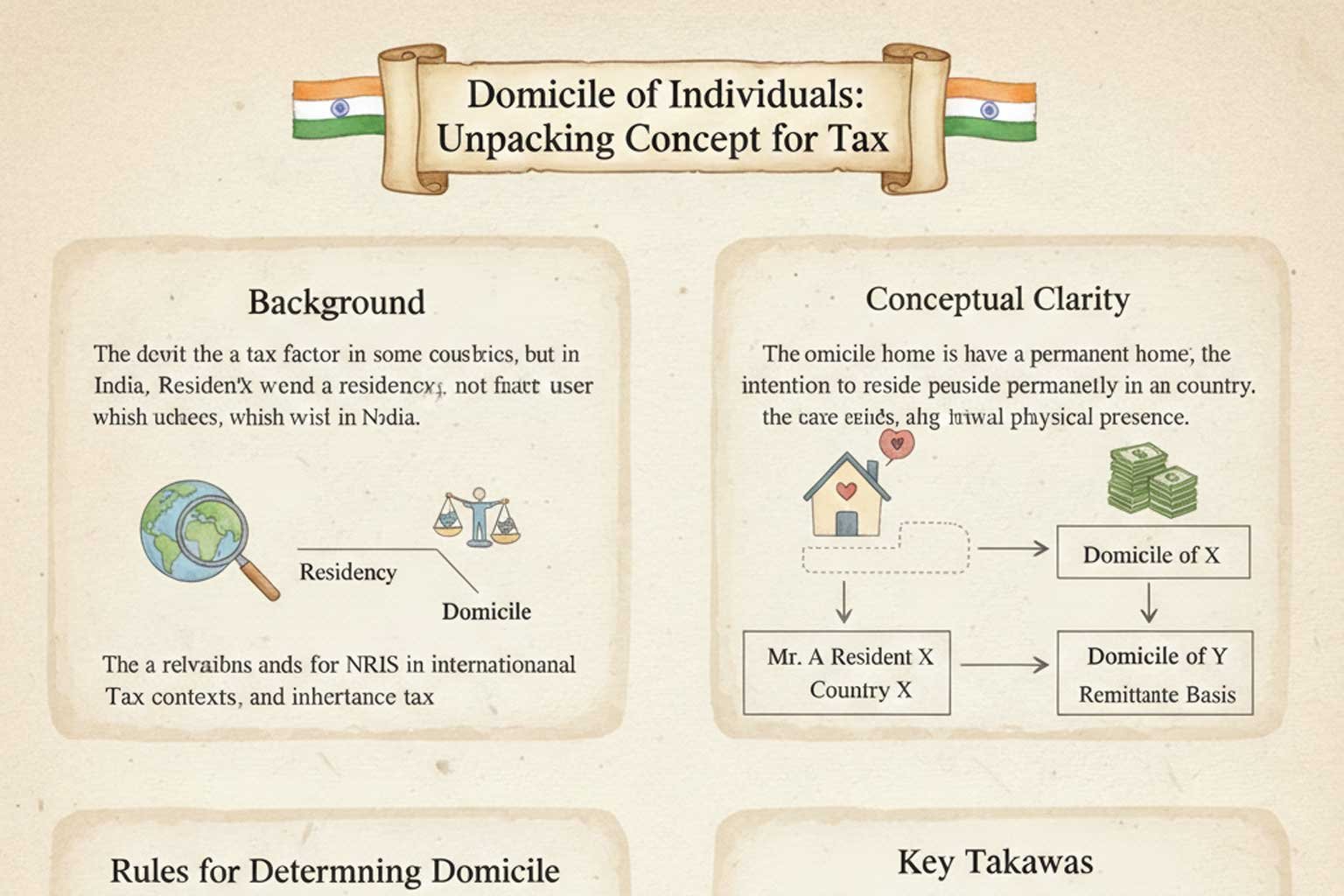

In certain countries, domicile of an individual is one of the factors for determining the scope of taxation of such individual in that country. In the Indian context, Income tax law does not recognise the scope of taxation on the basis of the domicile; rather it determines the scope of taxation only on the basis of the residency of an individual. This note does not deal with any specific country’s rules; but throws light on general principle of domicile and its connection with Income tax in certain countries. Though concept of domicile is not much relevant for Indian Income tax; however, in context of international taxation, sometimes it is pertinent to understand the taxation of the non-resident Indian in the other country which recognises the domicile principle for taxing the income.

It is important to note that a person may have a domicile which may or may not be in the same country as that of his residence (as per tax residency rule). The principle of domicile is much more permanent as compared to residency rules. Concept of domicile gains its importance in connection with inheritance tax (not leviable under Indian law till the date of publication of this note) in certain countries. In relation to Income tax, its relevance is for the treatment of certain foreign source income of an individual who is resident in a particular country however, domiciled in a foreign country.

Conceptual clarity on domicile

Generally, an individual would be considered to be a domicile of a particular country/state if he has permanent home in that country and such individual intends to permanently reside in that country. It is also imperative that such individual physically resides in that country. The country determining the scope of taxation of an individual, applies its system of laws to decide whether such domicile exists in that country or in a foreign country. The impact of domicile of an individual on his taxation could be understood with the help of an example.

Consider a situation where Mr. A is a tax resident of Country X and he derives income from Country X and Country Y. In this situation, Country X has to apply its system of tax laws to determine the domicile of Mr. A. In case he is domicile of State X, the taxation would be straight forward as most of the countries taxes its residents on the global income. However, in case Mr X is not the domicile of State X and Mr. A claim to be domicile of State Y, then the taxation of the income from State Y in State X has to be analysed as per the Income tax law of State X. In this situation, certain countries tax the income from State Y only if such income is remitted to the country where the individual is resident.

Rules for determining domicile

Generally, domicile could be determined effectively in two ways:

- Domicile by Birth

- Domicile by Choice

Domicile by Birth

A child on birth, automatically acquires the domicile of origin i.e. the domicile of the father. In case of the father’s death before birth or if the child is illegitimate, such child assumes the domicile of the mother.

In case parents are living apart, minor child acquires the domicile of the mother (which may or may not be same as that of father) if either of the below conditions are satisfied:

- The minor child is maintained by mother and has home with mother and has no home with father or;

- The minor child has attained the domicile of mother as per rule (i) above and since then, does not have home with father.

If the minor child acquires the domicile of the mother through either of the above rules, the minor child would continue to possess the domicile of the mother even on her (mother’s) death; provided the minor does not have home with his father since her death.

Note: None of the above rules alters the rule that the minor takes the domicile of his father in case where the parents are married and living together.

The minor continues to be domicile of origin till the attainment of age of majority. However, domicile of a minor may change if the father (or mother in some cases as discussed above) acquires new “domicile by Choice (refer below)”. In such case, the minor would continue to hold such domicile of choice till the age of majority. This is also known as “domicile of dependency”. If the minor (after attaining age of majority) subsequently abandons the domicile of dependency, then his domicile of origin automatically revives unless and until he acquires a new domicile by choice.

Domicile by Choice

Domicile by choice could be acquired only after attaining the age of majority. In order to acquire a domicile by choice, the individual after attaining the age of majority must move to a new country intending to make a permanent home there. Such individual must physically reside in the new country. It does not mean that he is required to cease his stay in the country of origin completely; however, the new country should be the principal place of residence.

When an individual abandons his domicile by choice then he automatically acquires the domicile of origin unless and until he acquires new domicile of choice.

Note: In some countries, domicile of a married woman is considered to be same as that of her husband and in contrast, some countries treat the married woman as separate person and acquire her domicile independently.

Key Takeaways

On the above backdrop, certain countries tax the foreign income of its residents only if they are remitted to such country in case the individual is domicile in that foreign country. Therefore, the onus is on the individual to prove the change in the domicile (from domicile of origin). Also, the most critical criteria to prove the domicile is the intention to permanently reside in that country and intention to make a permanent home there. It should also be backed by staying physically in such country. If the individual intends to return to the country of origin (based on facts) on the happening of a certain event which has a reasonable probability to occur, then he is likely to retain the domicile of origin.

This principle would be highly relevant in Indian context if the Indian legislation also intends to levy inheritance tax. Though Indian Succession Act, 1925 has reference to the concept of domicile; but the same is not concrete and clear. There is a need for a dedicated law relating to domicile.