This content is for Subscriber members only.

I don’t think so!

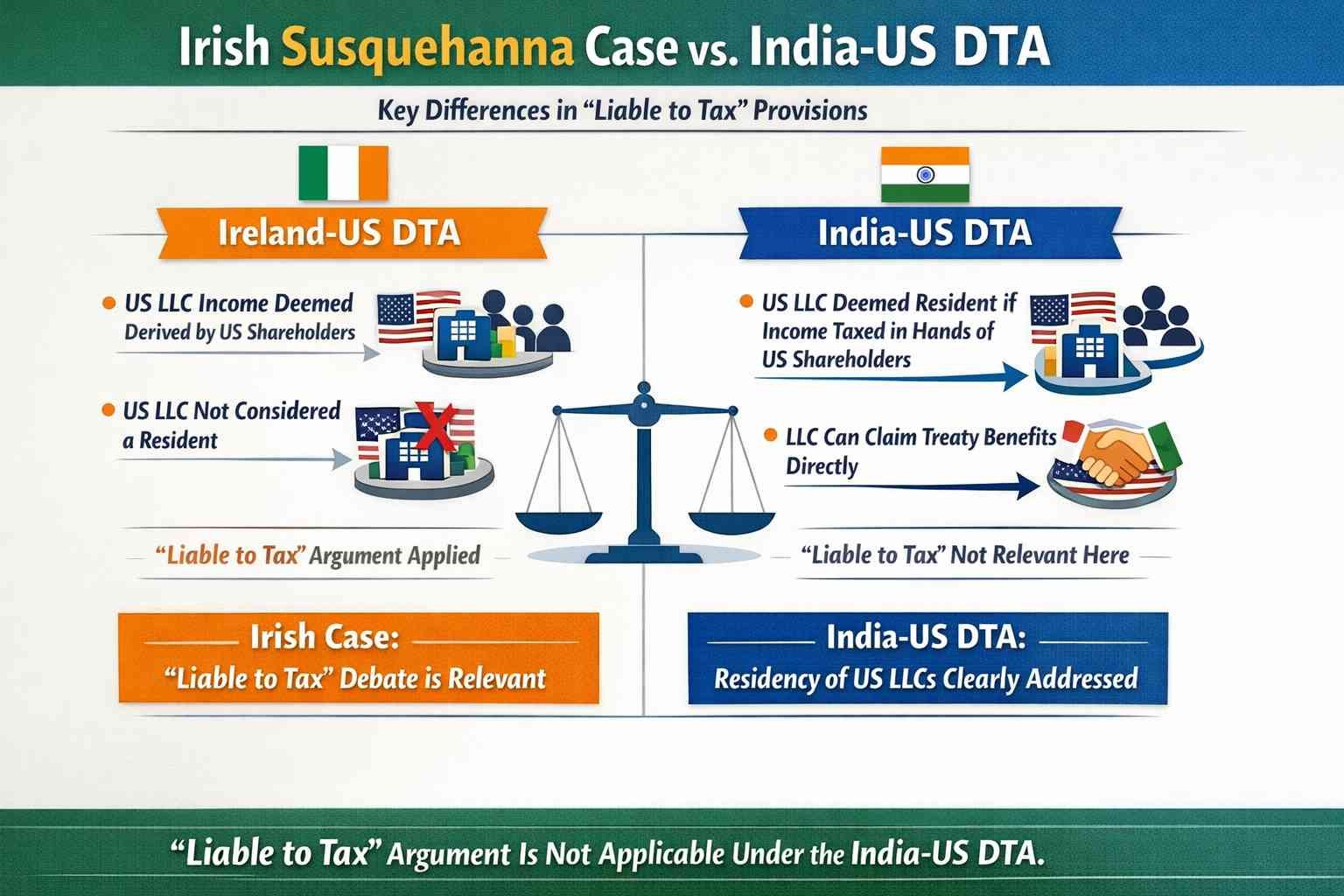

The key difference lies in the technical explanations of the India-US DTA and Ireland-US DTA.

According to the protocol and technical explanation of Article 4 of the Ireland-US DTA, income from a transparent entity (like a US LLC) is considered derived by its US shareholders if they are treated as US residents. Thus, US resident shareholders can claim treaty benefits, but the US LLC itself is not resident under Article 4 (as decided by the Irish court).

Conversely, article 4(1)(b) and the technical explanation of the India-US DTA deems the transparent entity (US LLC) itself as the resident in the US if the income is taxed in the hands of US resident shareholders. Therefore, the LLC can claim treaty benefits directly by virtue of article 4(1)(b) and satisfaction of the condition there, rendering the “liable to tax” argument purely academic for the India-US DTA.

Article 4(1)(b) of the India-US DTA specifically addresses the residency of transparent entities. If shareholders are US residents and subject to tax on the entity’s income, there is no need to further assess the “liability to tax” condition for the transparent entity itself. This is clarified in the technical explanation.

“Liable to tax” condition for the transparent entity must be satisfied only where there is no specific provision in the DTA dealing with the residency of such transparent entity and that is where the arguments related to “liable to tax” in the Irish court case would be relevant.

Although the Indian Tribunal in the case of General Motors arrived at the correct conclusion, the approach and principles relied on require reconsideration as they are not supported by evidence under US tax laws. I will deal with this in my next post.

#InternationalTax