This content is for Subscriber members only.

Is the decision on FTC correct? – Critical analysis

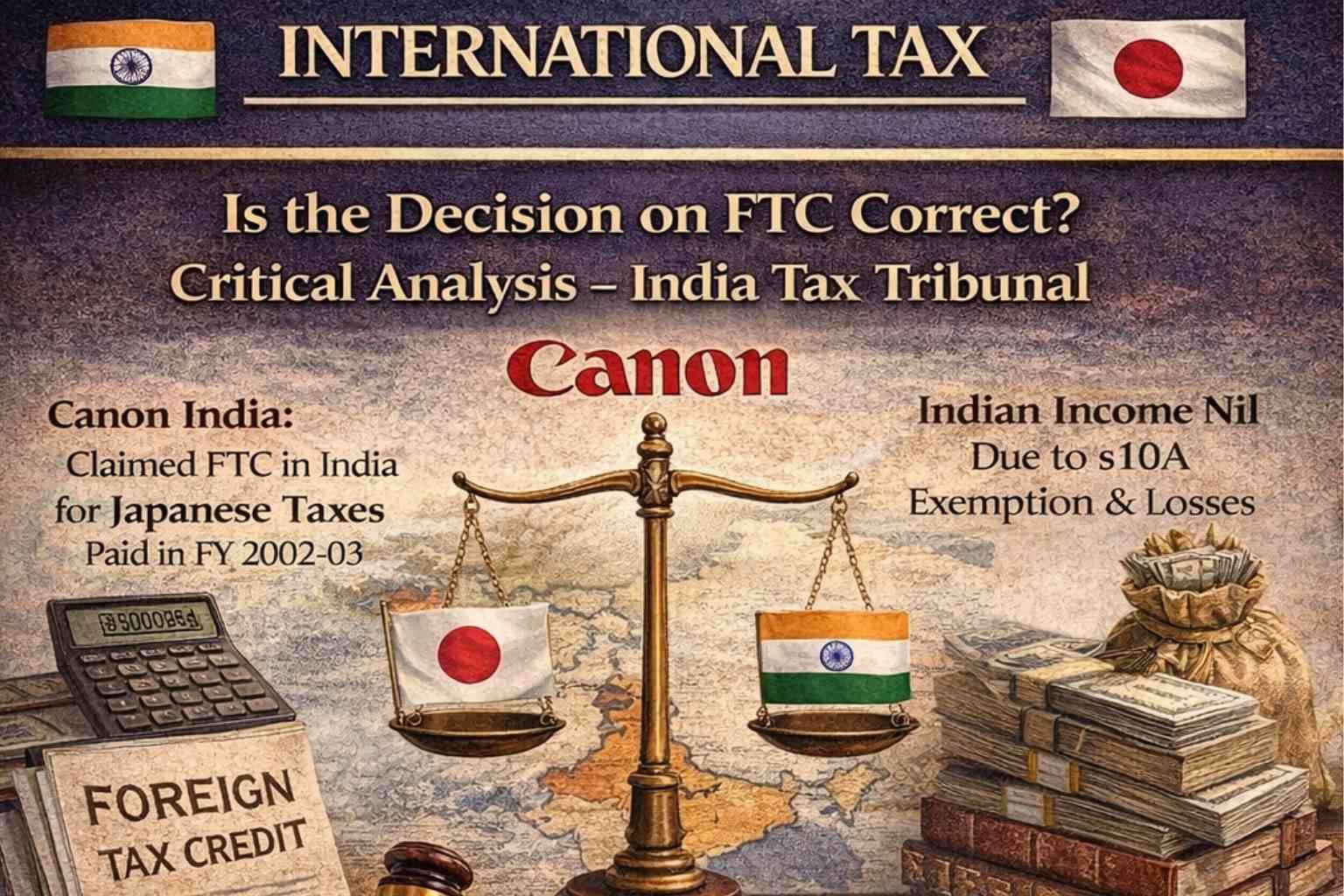

In the case of Canon India, the company was incorporated and considered a tax resident in India for the fiscal year 2003-04. The company earned certain income from operations in Japan, on which the Japanese tax authority withheld taxes. In India, the company claimed a foreign tax credit (FTC) on the total income earned from Japan. However, the taxable income in India was nil due to a specific exemption under Indian income tax law (s10A) as well as the company’s claim of losses.

The Indian Revenue Authorities (IRA) disallowed the full FTC. The Tribunal agreed with the taxpayer’s position and allowed the full FTC for taxes withheld in Japan, even though no income from Japan was taxed in India due to the exemption and loss claims. The Tribunal relied on a previous decision by the Delhi High Court, which in turn based its ruling on the Karnataka High Court’s decision in the Wipro case. Thus, analysing the Karnataka High Court’s decision is essential here.

In the Wipro case, the taxpayer relied significantly on an amendment to Section 90(1)(a)(ii). Prior to this amendment, India could enter into agreements with other countries to provide relief only when the taxpayer actually paid taxes in both the source state and India. However, after the 2004 amendment, India could enter into such agreements even if the income was merely chargeable to tax (but not actually paid) in the source country and India, as per their respective laws, to promote mutual economic relations, trade, and investment.

IRA argued that the FTC should not be allowed because the total income earned from Japan was exempt from tax in India, meaning no income was “chargeable to tax” in India. Nevertheless, the taxpayer successfully demonstrated through legal provisions and judicial precedents that income exempt under s10A of income tax law would still be treated as “chargeable to tax” in India. The taxpayer cleverly linked this argument of s10A “chargeability to tax” with the amendment to section 90 and submitted that this interpretation aligns with the amendment in Section 90, and consequently, the FTC should be fully allowed for taxes withheld in Japan.

In my opinion, two observations in the Wipro case merit reconsideration, as they could potentially alter the outcome:

- Linking the amendment in Section 90 with the language of Article 23 in existing treaties with India.

- Misinterpretation of the second sentence of Article 23 of the India-US and India-Japan DTAAs.

Regarding the first point, the amendment to Section 90 enables India to enter into agreements with any other country to provide relief if income is chargeable to tax under the laws of both jurisdictions, even if not actually paid. However, even after the amendment, the relief has to be allowed based on the article 23 language agreed between the countries. This amendment does not affect the language used in Article 23 of India’s existing treaties. Therefore, the credit under Article 23 must be determined based on the wording of that article in the relevant DTAA. The language employed in Article 23 closely mirrors that of the OECD/UN Model Treaty, which utilizes the ordinary credit method. According to the commentary and model treaty, the ordinary credit is the FTC, which shall not exceed the portion of Indian income tax attributable to income taxed in the other jurisdiction. As illustrated in the model treaty examples, no part of the Indian income tax would be attributed to income taxed in the other country if such income is either exempt in India or neutralized by losses. On this basis, the FTC would be nil, even if the computation mechanism under Section 91 were applied.

This argument that the amendment does not change the operative language of Article 23 was not raised by the IRA. IRA also did not point out that even after the amendment relief would flow through the specific language of the treaty. Accordingly, the maximum deduction or restriction on the FTC, provided in the second sentence of Article 23, must be adhered to, regardless of which computation mechanism is used. This restriction was not introduced or altered by the amendment and should not be interpreted as affected by the changes in Section 90.

With respect to the second point, it appears the High Court in the Wipro case misinterpreted the second sentence of Article 23 of the India-US DTAA by mixing it with timing mismatches, which is not applicable. Paragraph 62 of the OECD/UN Model Treaty commentary clarifies the interpretation of the second sentence of Article 23, prescribing the maximum deduction or restriction on the FTC. Based on this restriction, in the Tribunal’s present case, since no income tax is chargeable due to exemptions and losses, no portion of Indian income tax can be attributed to the foreign-sourced income, making the FTC nil.

In FY 2002-03, Canon India, a tax resident in India, earned income in Japan that was taxed at source. Although its Indian taxable income was nil due to s10A exemption and reported losses, Canon claimed a foreign tax credit (FTC) for Japanese taxes withheld. While the Indian Revenue Authorities (IRA) disallowed the FTC, the Tribunal allowed it, referencing Delhi and Karnataka High Courts’ decisions, notably the Wipro case [2016] 382 ITR 179.

The Wipro case centred on an amendment to Section 90(1)(a), which after 2004 permitted tax relief agreements even if income was merely “chargeable” but not actually taxed in both countries. IRA contended that exempt income under s10A was not “chargeable to tax,” but the taxpayer successfully argued that such exemptions still constituted “chargeability,” supporting their FTC claim under the amended Section 90.

In my opinion, two observations in the Wipro case merit reconsideration, as they could potentially alter the outcome:

- Linking the amendment in Section 90 with the language of Article 23 in existing treaties with India.

- Misinterpretation of the second sentence of Article 23 of the India-US and India-Japan DTAAs.

The amendment to Section 90 allows India to enter into agreements for tax relief with other countries, even if tax is not actually paid but the income is chargeable to tax in both jurisdictions. However, relief is still governed by the specific wording of Article 23 in each applicable DTAA with India, which generally follows the OECD/UN Model Treaty’s ordinary credit method. As per this model, FTC cannot exceed the portion of Indian tax attributable to the doubly taxed income. If the income is exempt in India or offset by losses, no FTC is available even if Section 91’s calculation were used.

This argument that the amendment does not change the language of Article 23 was not raised by the IRA. IRA also did not point out that the amendment was just an enabler and does not provide any relief in section 90 which has to be agreed specifically in article 23 of the treaty. Accordingly, the maximum deduction or restriction on the FTC, provided in the second sentence of Article 23, must be adhered to, regardless of which computation mechanism is used. This restriction was not introduced or altered by the amendment and should not be interpreted as affected by the changes in Section 90.

With respect to the second point, it appears the High Court in the Wipro case misinterpreted the second sentence of Article 23 of the India-US DTAA by mixing it with timing mismatches, which is not applicable. Paragraph 62 of the OECD/UN Model Treaty commentary clarifies the interpretation of the second sentence of Article 23, prescribing the maximum deduction or restriction on the FTC. Based on this restriction, in the Tribunal’s present case, since no income tax is chargeable due to exemptions and losses, no portion of Indian income tax can be attributed to the foreign-sourced income, making the FTC nil.