This content is for Subscriber members only.

Background

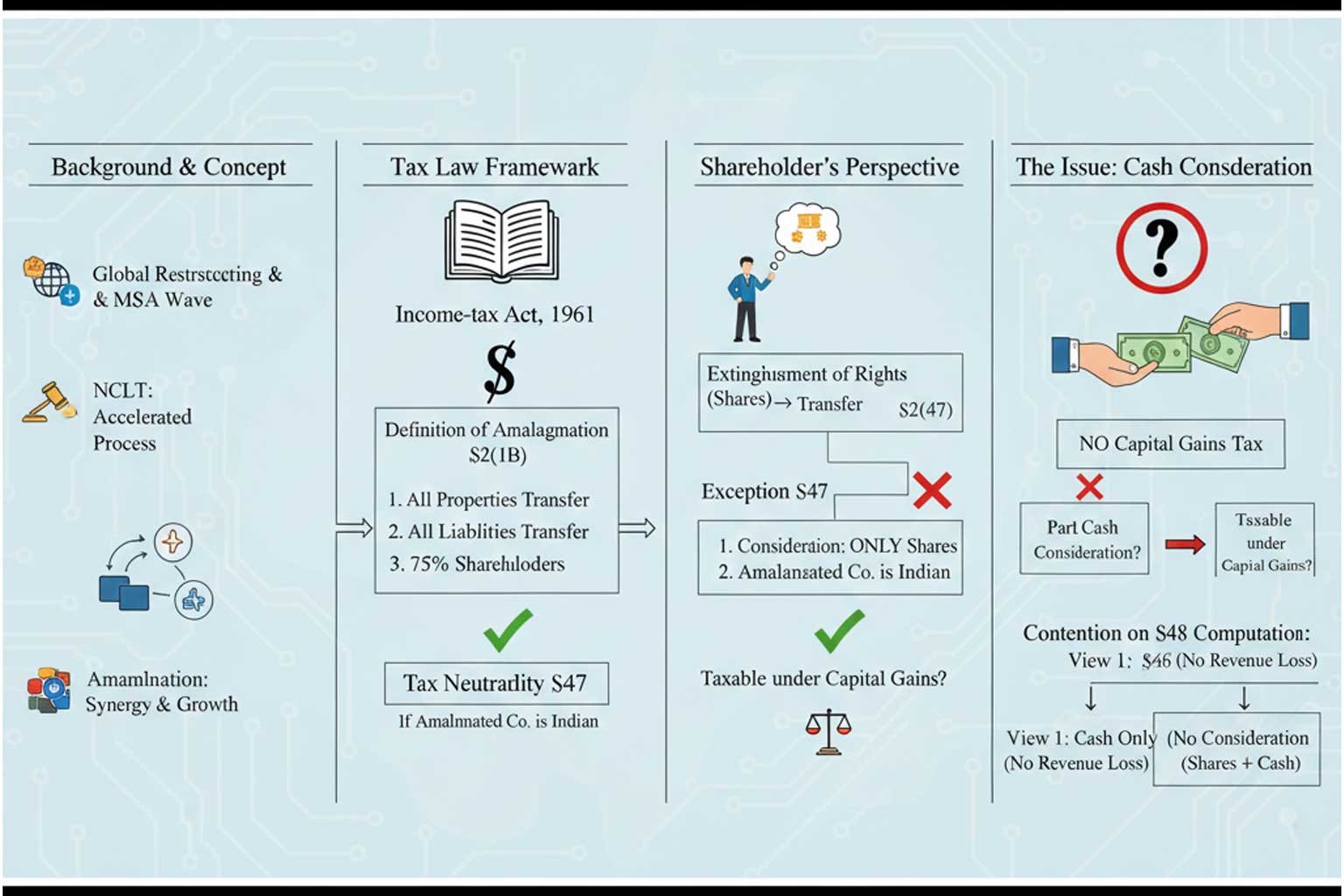

In the last couple of years, it may be perceived that corporates are devising ways to restructure their operations globally. A number of mergers and acquisitions are carried out around the world which leads to integration of their related entities in India. The basic idea behind mergers is to create synergy between different entities having strength in specific areas to boost the growth. Due to globalisation, India has also witnessed number of amalgamations and acquisitions in the last couple of years. Launch of National Company Law Tribunal has accelerated and eased the process of restructuring of corporates.

Amalgamation of corporates is one of the mode of restructuring by which either one or more corporate/s merge with an existing company or two or more corporates combine to form a new company. The regulatory provisions of amalgamation are laid down in the Company law in India. Several factors are analysed before restructuring the corporates out of which the most imperative variable is the commercial rationale on such restructuring. One of the other factors considered is the Income-tax exposure on such transaction (i.e. on amalgamation). The tax liability may be significant on amalgamation depending upon the amount of consideration and conditions laid down under Indian Income-tax law.

Relevant provisions of the Income-tax Act, 1961 (hereinafter referred to as “the Act”)

Amalgamation is defined in the Act[1] which lays down the following three conditions:

- All the properties of the amalgamating company become the property of the amalgamated company;

- All the liabilities of the amalgamating company become the liability of the amalgamated company;

- Shareholders holding 75% of the value of the shares of the amalgamating company become the shareholders of the amalgamated company.

Typically, amalgamation involves transfer of various capital assets (properties) of the amalgamating company to the amalgamated company for a consideration. Ideally, such transfer falls under the provisions of capital gains and liable to be taxed. However, by virtue of section 47, if all the conditions as referred above are adhered to, and if the amalgamated company is an Indian company, then such amalgamation transaction would be tax neutral. In other words, such transaction would not be treated as “transfer” and accordingly, would not be chargeable to tax in the hands of the amalgamating company (transferor).

From the point of view of shareholders of the amalgamating company, the ratio decidendi of the Hon’ble Supreme Court[2] is that the amalgamation results into extinguishments of rights in shares (of the amalgamating company) in the hands of the shareholders. Accordingly, “extinguishment of rights” falls under the purview of definition of ‘transfer’ under the provisions of the Act[3] and would be liable to capital gains tax in the shareholder’s hands.

However, again section 47 comes to the rescue of shareholders on such capital gains tax provided:

- Transfer of shares are made in consideration to allotment of share or shares of the amalgamated company;

- The amalgamated company is an Indian company.

Therefore, if the above conditions are satisfied, no capital gains would be taxable in the hands of the shareholders.

Issue for consideration

- Whether part consideration to the shareholders in the form of cash would violate the condition (a) above and results into capital gains tax in the hands of the shareholders?

- If the answer to the above is yes, whether consideration for the purpose of section 48 would be restricted to the extent of cash component?

With reference to the issue no. (a) above, it is crystal clear from the provision of the Act[4] that consideration shall be by way of allotment of share/s. Part consideration in cash would indubitably violate the provisions and consequently, taxable under the head capital gains.

With reference to the issue no. (b) above, ambiguity in the provision has caused divergent views as follows:

View 1 – Consideration, only to the extent of cash should be considered for the purpose of section 48

The arguments in favour of this view are as follows:

- Considering only cash component as the full value of consideration would not lead to any revenue loss to the exchequer. This aspect may be comprehended with the help of an example:

Example: A company ABC Pvt. Ltd. (amalgamating company) merged with XYZ Pvt. Ltd. (amalgamated company) under the scheme of Amalgamation approved by NCLT effective in FY 2019-20. Amalgamating company had 1,00,000 shares of INR 10 each amounting to share capital of INR 10,00,000. Two shareholders “A” and “B” of amalgamating company held 60,000 and 40,000 shares respectively. The consideration of amalgamation was agreed at INR 1 Crore of which 25% was decided to be remitted in cash and remaining 75% was in the form of allotment of shares in amalgamated company. It was also agreed in the scheme of amalgamation that consideration for each share of amalgamating company is INR 100 and the shareholders will receive one share of amalgamated company for each share of amalgamating company. In other words, the value of each share of the amalgamated company is INR 100. Accordingly, shareholder “A” will receive 45,000 shares of amalgamated company of INR 100 each amounting to INR 45,00,000. Also, cash amounting to INR 15,00,000 being value of 15,000 shares. The shares in the amalgamating company are short term capital assets in the hands of the shareholder “A”. The capital gain computation in this scenario would be as follows:

S. No | Particulars | Scenario 1 – Cash component | Scenario 2 – Total consideration |

A | Full value of consideration | 15,00,000 | 60,00,000 |

B | Less: cost of transfer | NIL | NIL |

C | Net consideration (A-B) | 15,00,000 | 60,00,000 |

D | Less: cost of acquisition | 1,50,000 (15,000 shares of 10 each) | 6,00,000 (60,000 shares of 10 each) |

E | Short term capital gains (C-D) | 13,50,000 | 54,00,000 |

Note: All the above referred figures are in Indian Rupee

Suppose, Shareholder “A” transfers the total shares of amalgamated company (i.e. 45,000 shares) in the FY 2020-21 for INR 200 per share, the computation of capital gains in both the above scenarios would look like as below:

S. No | Particulars | Scenario 1 – Cash component | Scenario 2 – Total consideration |

A | Full value of consideration (45,000 x 200) | 90,00,000 | 90,00,000 |

B | Less: cost of transfer | NIL | NIL |

C | Net consideration (A-B) | 90,00,000 | 90,00,000 |

D | Less: cost of acquisition (45,000 shares of 10 each) | 4,50,000 | 45,00,000 |

E | Short term capital gains (C-D) | 85,50,000 | 45,00,000 |

Note: All the above referred figures are in Indian Rupee

It may be observed from the above computation that the total capital gains is same in both the scenarios i.e. INR 99,00,000 (i.e. INR 13.5 Lakh + INR 85.5 Lakh in Scenario 1 and INR 54 Lakh + INR 45 Lakh in Scenario 2). In other words, there is no loss to the revenue even if only cash component is considered as full value of consideration as on the year of transfer as higher tax would be required to be paid in the future when the shares of the amalgamated company are transferred.

The same principle applies even if the shares of the amalgamating company is a long-term capital asset. Though the amounts may not match in both the Scenarios (due to difference in period of indexation), still the tax will be more in the future when the shares of the amalgamated company are sold (similar to Scenario 1 in above table). In light of the above example, the view seems to be logical.

- The definition of amalgamation does not prohibit a part of consideration in cash.

The definition of amalgamation[5] is discussed earlier in this article wherein no prohibition exists for part of the consideration in cash. One of the conditions stipulate that the shareholders holding 75% of the value of shares becomes the shareholder of the amalgamated company. To put it differently, even if the shareholder of the amalgamating company (holding 75% value of shares) receives a single share of the amalgamated company, the condition prescribed is satisfied.

- The language of section 47(vii)of the Act is not strictly worded.

Further, wherever the legislation has sought to specifically prohibit the consideration in any form other than shares, the law was drafted evidently to capture this aspect. One of such example is section 47 (xiii) wherein one of the conditions for tax neutral conversion of a firm into a company is that the partner of the firm does not receive consideration in any form other than by way of allotment of shares of the company. The relevant extract of the section is produced below for ready reference:

“any transfer of a capital asset or intangible asset by a firm to a company as a result of succession of the firm by a company in the business carried on by the firm, or any transfer of a capital asset to a company in the course of demutualisation or corporatisation of a recognised stock exchange in India as a result of which an association of persons or body of individuals is succeeded by such company :

Provided that—

(a)……………………………

(b)……………………………

(c) the partners of the firm do not receive any consideration or benefit, directly or indirectly, in any form or manner, other than by way of allotment of shares in the company; and

(d)…………………………….

(e)……………………………..”

Section 47 (xiv) also instructs similar requirement wherein one of the conditions for tax neutral conversion of proprietorship into a company is that the proprietor does not receive consideration in any form other than by way of allotment of shares of the company. The relevant extract of the section produced below for ready reference:

“where a sole proprietary concern is succeeded by a company in the business carried on by it as a result of which the sole proprietary concern sells or otherwise transfers any capital asset or intangible asset to the company:

Provided that—

(a)……………………………

(b)……………………………

(c) the sole proprietor does not receive any consideration or benefit, directly or indirectly, in any form or manner, other than by way of allotment of shares in the company;”

In the above backdrop, the language incorporated in the law under section 47(vii) of the Act is different from the above referred sections. The relevant extract of the section produced below for ready reference:

“any transfer by a shareholder, in a scheme of amalgamation, of a capital asset being a share or shares held by him in the amalgamating company, if—

(a) the transfer is made in consideration of the allotment to him of any share or shares in the amalgamated company except where the shareholder itself is the amalgamated company, and

(b) ……………………………………”

On perusing the above highlighted portion, section 47(vii) does not emphasize on the point that the total consideration must be in the form of the shares and could not compose cash or any other form. However, provisions of section 47(xiii) and 47(xiv) specifically stress on this aspect which is apparent from the language used in the provision. Accordingly, the view that the consideration may be constituted with cash component, gains weight from this argument.

- Exemption provisions should be construed liberally

It is a well settled principle that beneficial provisions to the assessee, should be construed liberally. Especially, provisions for exemption, deduction or relief should be liberally interpreted so as to provide benefit to the taxpayers. This is for the reason that legislature enacted exemption provisions for the benefit of the people and to avoid genuine hardship to the general public. Reading such provisions strictly would be contrary to the intention of the legislature and will not achieve the purpose for which it was enacted. The exemption provision has to be interpreted so as to advance the objective of the provision and not to frustrate it. There are plethora of judgements of the Hon’ble Supreme court[6] and various high courts on this facet.

Therefore, the argument on the basis of the above principle is that section 47 provides exclusion from transfer thereby exempting a particular transaction from capital gains tax. Accordingly, the provisions in section 47 has to be construed liberally and in case consideration consists of cash component, only such component should be considered as full value of consideration.

View 2 – Total consideration (including shares and cash component) should be considered for the purpose of section 48

The arguments in favour of this view are as follows:

- Conditions of the exemptions provisions has to be construed strictly

As discussed earlier in this article, there are catena of decisions of the various high courts deciding that exemption provisions have to be interpreted liberally as it is intended to provide benefit to the taxpayers and accordingly, hyper technical or pedantic reading of the exemption provisions is not warranted. However, it is highly pertinent to note that the recent decision of the Hon’ble Supreme Court[7] related to the matter of customs, has laid down a very important ratio in connection with the exemption provisions.

The Hon’ble Court has decided that the conditions listed out in any exemption provisions has to be strictly adhered to. The conditions of the exemption provisions could not be read liberally. Such exemption should be allowed to be availed only to those subjects/assesses who demonstrate that a case for exemption squarely falls within the parameters enumerated in the exemption provision/notification. If the taxpayer satisfies all the conditions laid down in order to avail the exemption, only in such cases the taxpayer would be allowed to take the shelter of the exemption provisions. The Hon’ble Supreme Court also ruled that any aspects other than the conditions, could be interpreted generously. Therefore, any procedural aspects to avail the exemption has to be read in such a way to make it workable. In other words, highly technical reading of the procedural matters should not deprive the benefit to the taxpayers. This ratio was also laid down in the context of Income-tax by the Hon’ble Supreme Court in the case of Prabhakar P. R[8].

In light of the above, one of the conditions laid down in section 47(vii) to move out of the rigours of “transfer” is that the shareholder’s consideration should be in the form of allotment of share/s in the amalgamated company. There is no whisper of any other mode of consideration in this section. Accordingly, in view of the Supreme court decision (supra), this condition has to be construed strictly and there is no scope of reading the provisions to read as part consideration could be in the form of cash and still the exemption would be available to the extent of consideration in shares.

- The plain language used by the legislature could not be altered unless it throws absurd results.

It is a well settled principle that unless there is an intention to the contrary, the words in the statue should be given their ordinary grammatical and natural meaning[9]. The literal rule of statutory interpretation demands that if the statue is plain, the courts must apply it irrespective of the consequences[10]. The plain language of the statue must override any supposed intendment of the legislature and cannot be altered or stretched by the court[11]. One should squarely look at the words in the light of what is expressly stated and nothing can be implied so as to supply any assumed deficiency[12].

Statutory principle of interpretation also demands that no words should be added or subtracted, or altered or modified unless it is plainly necessary to do so in order to prevent a provision from being unintelligible, absurd, unreasonable, unworkable or totally irreconcilable with the rest of the statue[13]. The language employed in the statue is the determinative factor of legislative intent and even assuming there is a defect or any omissions in the words used in the legislation, the courts cannot correct or make-up the deficiency, especially when a literal reading thereof produces an intelligible result. Any departure from the literal rule would really be amending the law in the garb of interpretation which is not permissible and which would be destructive of judicial discipline[14].

In the backdrop of above principles, it may be noted that the language of section 47(vii) is plain and unambiguous. The condition specifically lays down that the transfer by the shareholder in the scheme of amalgamation would be tax neutral if the transfer is made in consideration of the allotment of share/s in the amalgamated company. The language is so clear that there could not be any assumptions or presumptions to this condition. Argument that in case of part consideration in cash, the taxable consideration would be only to the extent of cash component, would lead to a supposed intendment of the legislature and also imply altering the provision of the act which is not permissible.

The language is very clear so as to provide intelligible result. The legislation specifically provides the transfer by shareholders as exempt transfer if the consideration is in the form of allotment of share/s. Argument that the definition of amalgamation does not prohibit cash consideration would not stand as the provision of section 47(vii) specifically relates to the transfer by the shareholders and it provides that the consideration should be in the form of allotment of share/s. This condition has to be construed strictly as laid down by the Hon’ble Supreme Court (supra). The intention also seems to provide exemption to the shareholders if the consideration is in the form of shares and the amalgamation transaction is not a mere device for repatriation of cash of the amalgamating company so as to avoid the dividend distribution tax in the hand of the amalgamating company.

Interpretation to tax only the consideration to the extent of cash would lead to alteration and stretching the general meaning of the language incorporated in the section 47(vii) though such plain language does not provide any absurd results. Such an interpretation would be against the statutory principles of interpretation. Even if it is assumed that there is a deficiency in the provision to the extent that it does not provide for exempt transfer to the extent of consideration in shares, such deficiency could not be enforced by the judiciary as it would amount to amending the law which is against the judicial discipline. Though the language incorporated in section 47(vii) is not the same as in the provisions of section 47(xiii) and 47(iv) (referred earlier in this Article), it would not mean that the words used throws absurd results.

In addition to the above, section 47 enumerates the transactions which would not be treated as transfer. This obviously means that if the conditions specified in the provision are not satisfied, then the transaction would be treated as transfer and the provisions of section 48 (computation mechanism) and other provisions would be attracted so as to tax such transaction as capital gains/loss. Indubitably, part consideration in the form of cash would breach the provisions of section 47(vii) and accordingly, such transfer of shares by the shareholders of the amalgamating company would be regarded as transfer and would be liable to capital gains tax subject to the provisions of section 48. Nowhere in section 48 prescribes for bifurcation of the consideration into cash and share component and tax only one of them as contemplated in view 1 (supra). Accordingly, taxing only cash component would amount to rewriting the law again which is impermissible.

- Deferment of tax is impermissible even if there is no loss to the revenue in future

The provisions of the Act states that the income is required to be taxed in the year in which it is received, deemed to be received, accrue or arise or deemed to accrue or arise in the hands of a resident. Generally, income accrue or arises when the right to receive the income is established. Also, the charging section of capital gains stipulates that any profits or gains arising from the transfer of a capital asset would be chargeable to tax under the head capital gains in the year in which such transfer took place. It is very clear that capital gains/loss could not be postponed if the transfer took place in a previous year. Therefore, the plea that the exchequer would not loose any revenue in the future even if the capital gains are postponed is contrary to the provisions of the Act and bad in law.

- CIT v. Gautam Sarabhai Trust [1988] 173 ITR 216 (Guj)

The Hon’ble Gujarat High Court, in the above referred case, had dealt with section 47(vii) and ruled that the consideration contemplated in the section is nothing but share or shares only in the amalgamated company. It is not necessary to add or read ‘only’ in sub clause (a). If besides the share or shares in the amalgamated company, the shareholder of the amalgamating company is allotted something more, say bonds or debentures, in consideration for the transfer of his share or shares in the amalgamating company, he cannot get the benefit of section 47(vii). Composite consideration is not contemplated by section 47(vii)(a).

In light of the above case, the same analogy may also be imported with respect to the part of consideration in cash. Accordingly, even if cash is one of the components of the consideration, benefit of section 47(vii) would not be available.

Conclusion

In the backdrop of detailed arguments on both the views, it is important to analyse the well settled principles of taxation and then arrive at the objective which is intended by the legislation to achieve.