This content is for Subscriber members only.

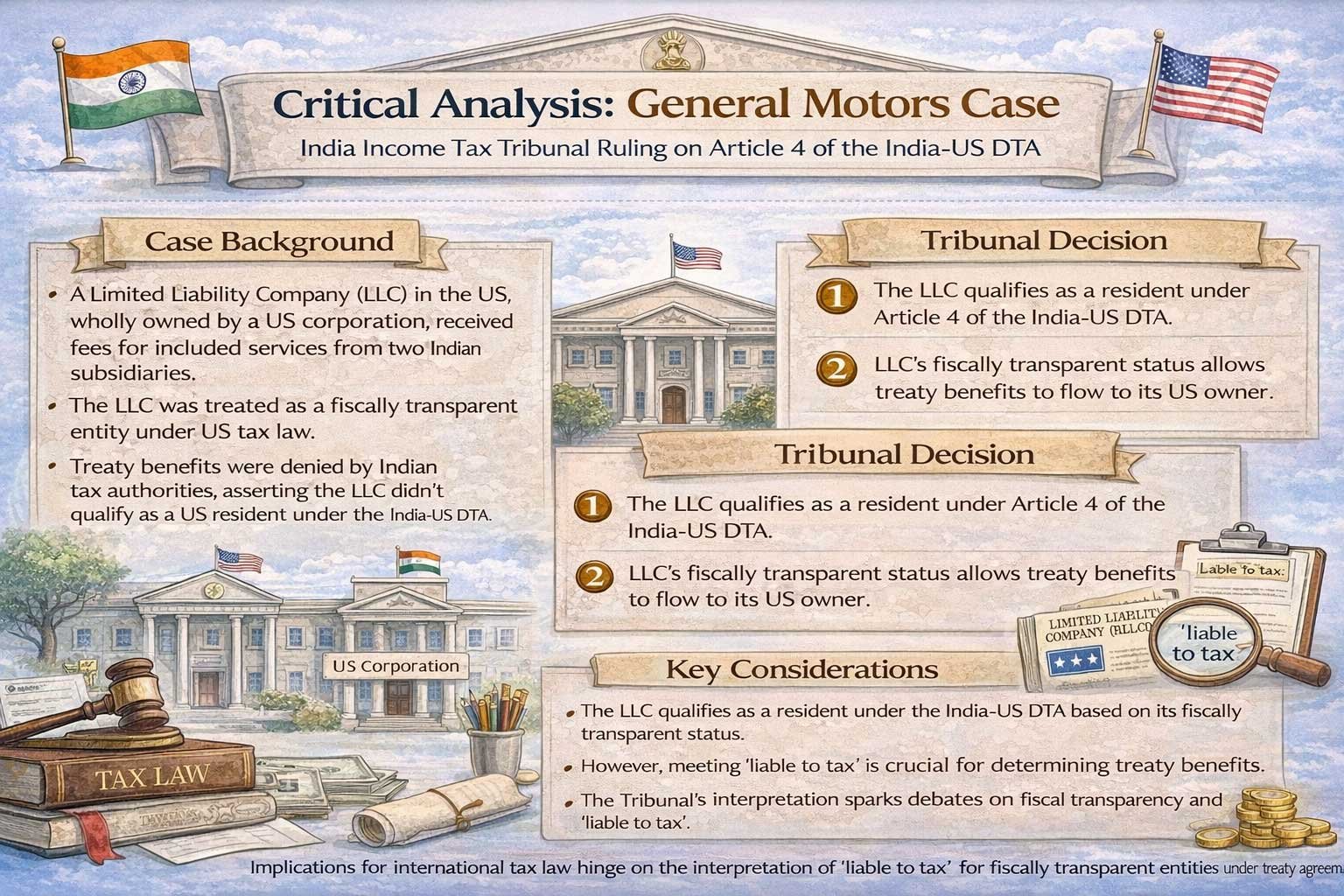

Critical Analysis – General Motors case[1] of India Income Tax Tribunal on Article 4 of India-US DTA

Brief Facts of the Case:

A Limited Liability Company (LLC) was incorporated in the US and was wholly owned by a US corporation, qualifying as a resident under US corporate tax law. The LLC was treated as a fiscally transparent entity per US corporate tax regulations. It received fees for included services from two Indian subsidiaries, but these fees were taxed at a higher rate by the Indian income tax authorities due to denial of treaty benefits. The primary grounds for denying treaty benefits were:

- The LLC was not liable to tax in the US and thus did not qualify as a resident under Article 4 of the India-US Double Taxation Avoidance Agreement (DTA).

- The LLC was not specifically mentioned in Clause 1(b) of Article 4 of the India-US DTA, resulting in its exclusion from treaty residency.

Issue for Resolution:

The main issue before the Tribunal was whether the LLC qualified as a resident under Article 4 of the India-US DTA, thereby entitling it to treaty benefits.

Tribunal Decision:

Relevant paragraphs of the Tribunal’s reasoning are found in paragraph 4 of the decision, which contains eight sub-paragraphs elucidating the basis for concluding that the LLC is a resident under Article 4 of the India-US DTA and eligible for treaty benefits.

In paragraphs 4.2 and 4.3, the Tribunal referenced the tax residency certificate (TRC) obtained by the LLC, citing its language:

“I certify that, to the best of our knowledge, the above-named Limited Liability Company is a branch, division, or business unit of a U.S. corporation that is a resident of the United States of America for purposes of U.S. taxation.”

The Tribunal noted in paragraph 4.2 that, for fiscally transparent entities, a US residence certification merely certifies that the entity submitted an information return and that its partners/members/owners/beneficiaries filed returns as US residents. The TRC indicated that the LLC was a branch of the US corporation (the owner), which is resident in the US, rather than the LLC itself being recognized as resident.

A TRC analysis shows that for the LLC to be considered resident under Article 4, two conditions must be met, its owner (a US corporation) is US-resident and the LLC’s income is “subject to tax” in the owner’s hands. Though the first condition seems to be satisfied based on the TRC, there is no finding or documentary evidence recorded by the Tribunal that the LLC’s income was taxed at the parent level, so the TRC alone is insufficient to establish LLC residency under Article 4.

In paragraph 4.5, the Tribunal revisited the TRC and asserted that the LLC is considered resident under Article 4 by virtue of incorporation and separate legal existence as a ‘person’. However, it should be noted that mere incorporation under US law does not suffice; Article 4 requirements must be met. The Tribunal relied on the principle established in Green Emirates Shipping and Travels[1], observing that a person with locality attachments (such as fiscal domicile via incorporation) triggering residence-type taxation should be treated as resident, a status independent of actual tax imposition. The ITAT Mumbai case of Linklaters LLP[2] was also cited in support of this view.

Nevertheless, this principle remains untested by the Supreme Court of India and is not clearly articulated in OECD/UN Commentaries. Indeed, the OECD commentary often indicates that fiscally transparent entities are not liable to tax in their own right, a point highlighted by the Dispute Resolution Panel (DRP).

In paragraph 4.4, the Tribunal stated that the LLC is liable to tax because US corporate tax law permits the LLC to elect to be a taxable entity or not. It is difficult to understand how mere the option to elect can be conclusive of the fact that the LLC is “liable to tax”. In my view the effect of such election must be considered. If the LLC elects non-taxable status, then it is not liable to tax; if it elects taxable status, then it is. Thus, the Tribunal did not establish broad principles in this regard.

Further, there were no documentary evidence within the decision substantiating how taxable income and corporate tax are computed for the LLC. The decision did not clarify whether the computation occurs at the LLC level and then is attributed to the owner or is directly consolidated with the owner’s income. In cases where income is attributed entirely to the owner, it is difficult to conclude that the LLC itself is liable to tax. The Tribunal did not discuss mechanisms of income attribution or tax computation in detail as per the US corporate tax law.

The comparability between US consolidated group rules and the tax treatment of a disregarded LLC entity was also not substantiated. Consequently, assertions that the LLC is liable to tax because the income is attributed to and discharged by the owner lacked supporting evidence or analysis of the computational mechanism.

Paragraph 4.7 addressed Article 4(1)(b) of the Treaty but did not offer a definitive principle. The Tribunal observed:

“We are of the considered view that the intent of the Indo-US Treaty has to be given precedence wherein the concept of fiscally transparent entity is the recognized way of recognizing the phrase ‘liable to tax.’ The fact that paragraph 1(b) of Article 4 of the Indo-US Tax Treaty recognizes partnership as a resident of the US for the purpose Indo-US Treaty to the extent that the income derived by such partnership is subject to tax in the US as the income either in the hands of the partnership or in the hands of its partners or beneficiaries. In this context, the judgement of the Mumbai Tribunal in the case of Linklaters LLP vs. ITO (supra) can be relied”

Paragraph 4.8 discussed the “subject to tax” criterion concerning LLC income in the US, however, lost somewhere discussing the inclusion and exclusion approach, stating:

“Further, we also find force in the contention of the ld. Sr. Counsel that this provision imposes a limitation on eligibility of a partnership to avail the benefits of India-US tax treaty as prescribed, i.e., it seeks to exclude from the eligibility of provisions of India-US tax treaty such income of the partnership which is not ‘subject to

tax’ in the US (either in the hands of partnership or partners). Reliance in this regard can be placed on ruling by AAR in case of General Electric Pension Trust vs DIT[1]. In this consideration of the matter, it can be concluded that that an exclusion provision can only exclude something if it was included at the outset. Hence, a fiscally transparent partnership was already regarded as ‘liable to tax’ for the purposes of India-US tax treaty and this provision determines the scope of eligibility of such fiscally transparent partnership by excluding income which is not ultimately ‘subject to tax’ in the US”

Analysis:

Based on the tribunal’s discussion, it focused primarily on whether the LLC is “liable to tax” to meet the requirement for residency under Article 4. This prompts the question, is it necessary to prove liability to tax to establish residency under Article 4, or can residency be demonstrated independently of this condition?

In my assessment, Article 4(1)(b) and the technical explanation within the India-US Treaty are critical. Article 4(1)(b) provides a specific provision concerning fiscally transparent entities and outlines a self-contained framework for determining residency. The relevant text states:

“1. For the purposes of this Convention, the term “resident of a Contracting State” means any person who, under the laws of that State, is liable to tax therein by reason of his domicile, residence, citizenship, place of management, place of incorporation, or any other criterion of a similar nature, provided, however, that

(a) ……………………….

(b) in the case of income derived or paid by a partnership, estate, or trust, this term applies only to the extent that the income derived by such partnership, estate, or trust is subject to tax in that State as the income of a resident, either in its hands or in the hands of its partners or beneficiaries”

Further the relevant para of the technical explanation is reproduced below:

”Under paragraph l (b), a partnership, estate or trust will be treated as a resident of a Contracting State for purposes of the Convention to the extent that the income derived by such person is subject to tax in that State as the income of a resident, either in the hands of the person deriving the income or in the hands of its partners or beneficiaries. Under U.S. law, a partnership is never, and an estate or trust is often not, taxed as such. Under the Convention income received by a partnership, estate or trust will be treated as income received by a U.S. resident only to the extent such income is subject to tax in the United States as the Income of a U.S. resident. Thus, for U.S. tax purposes, the question of whether income received by a partnership is received by a resident will be determined by the residence of its partners rather than by the residence of the partnership itself. To the extent the partners (looking through any partnerships which are themselves partners) are subject to U.S. tax as residents of the United States, the income received by the partnership will be treated as income received by a U.S. resident.”

The technical explanation reinforces that under paragraph 1(b), a partnership, estate, or trust qualifies as a resident to the extent its income is subject to tax in the hands of US

resident shareholders or partners. Therefore, a US LLC can claim treaty benefits directly if its income is taxed in the hands of its US-resident owners, making the “liable to tax” discussion largely academic regarding the India-US DTA.

Accordingly, Article 4(1)(b) expressly addresses the residency of transparent entities. If the owners are US residents and are subject to tax on the entity’s income, further inquiry into the transparent entity’s “liability to tax” is unnecessary. This interpretation is supported by both the treaty text and technical explanations.

“Liable to tax” condition for the transparent entity must be satisfied only where there is no specific provision in the DTA dealing with the residency of such transparent entity and that is where the arguments related to “liable to tax” would be relevant.

With respect to argument on “liable to tax”, it is relevant to look at the recent decision of the Irish Court of Appeal in the case of Susquehanna[1] where the court ruled that the US LLC is not a resident under Article 4 as it is not “liable” to tax in the US. The taxpayer placed heavy reliance on the TD Securities case[2] under the US-Canada DTA, where the Canadian court ruled that the USA LLC is a resident under the DTA as it is ultimately liable to tax in the hands of its shareholder, which was a corporation. However, the Irish court distinguished this case on two points:

- The TD Securities case was based on a finding that the income of the US LLC was subject to full and comprehensive taxation in the hands of a corporation. However, in the current case, the US LLC income was ultimately taxed in the hands of individuals and not a corporation. Thus, it could not be proven that the same tax as that of a corporation was paid by the individuals.

- The reasoning and conclusion in the TD Securities case were firmly rooted in U.S. and Canadian interpretation and practice, which could not be proven in the context of Ireland and US interpretation and practice.

Further, the Irish court strongly emphasized that it is the person who is required to be liable to tax under Article 4, and not the income. In other words, the US LLC (person) was not liable to tax, although the income of the US LLC was ultimately taxed in the hands of its ultimate owners, who were individuals.

Conclusion:

For US fiscally transparent entities, Article 4(1)(b) of the India-US DTA provides a clear standard for determining residency. Where such an entity’s income is subject to tax in the hands of its US-resident owners, the entity may be considered a resident under Article 4, and the “liable to tax” requirement is rendered moot. The “subject to tax” standard is more rigorous than simple “liability to tax,” so fulfilling the former inherently satisfies the latter for the owners.

Though the Tribunal came to the correct conclusion, its decision did not sufficiently emphasize the principles contained in Article 4(1)(b) and its technical explanation, nor did it robustly analyse or substantiate its reasoning with relevant and corroborative documentation.