This content is for Subscriber members only.

Is the interpretation of TAC correct?

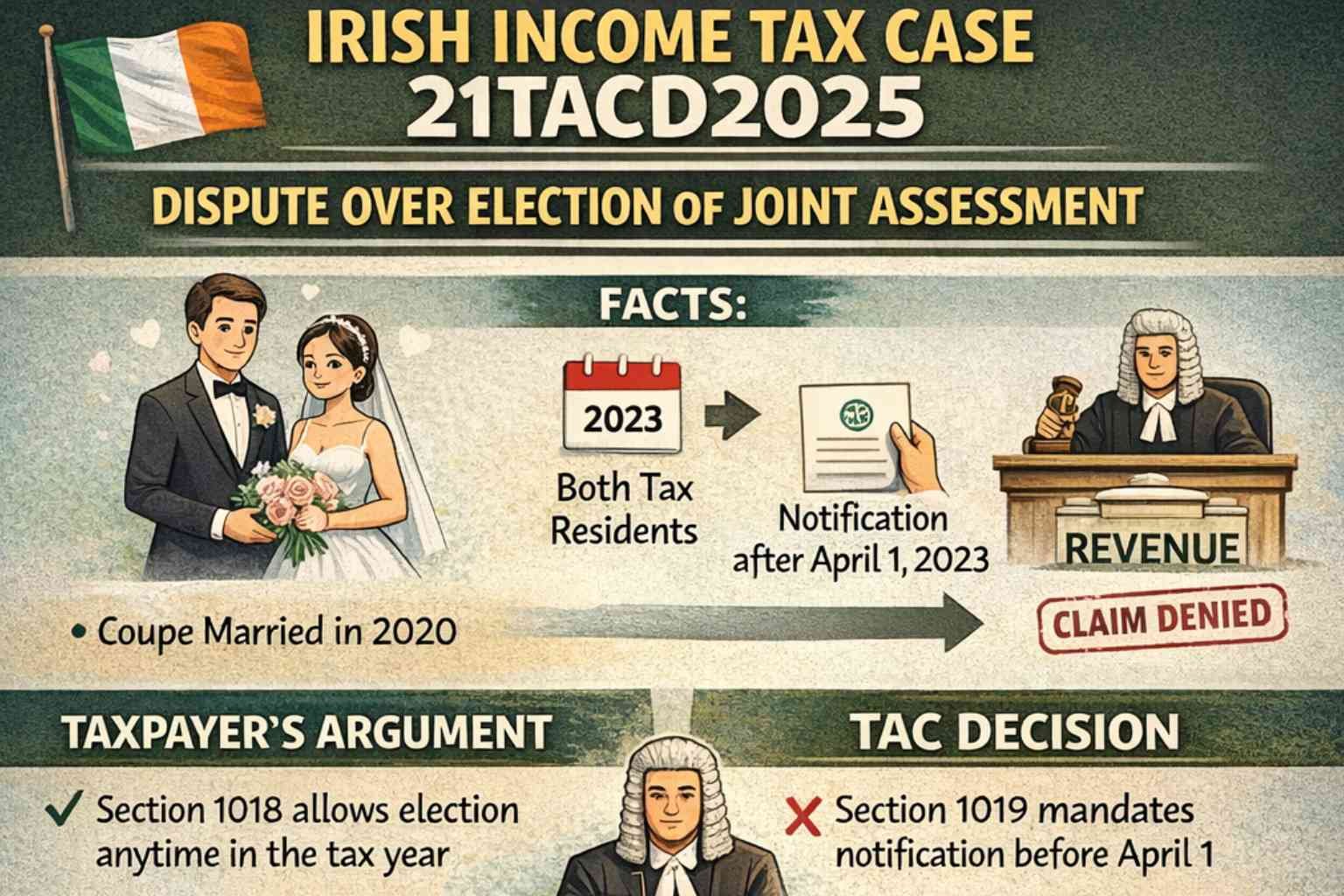

Facts: The appellant got married in 2020, and the spouse(wife) was a non-resident of Ireland from 2020 to 2022. The appellant and the spouse were tax residents for the current tax year 2023. The appellant notified the revenue to elect for the joint assessment, with the appellant as the assessable spouse, after 1st April 2023. The revenue denied the claim for joint assessment on the grounds that the notification for election of joint assessment was not given before 1st April 2023 and applied separate treatment under section 1016.

Appellant’s Submission: Section 1018 provides for the election of joint assessment at any time during the tax year. There is no requirement to notify the revenue before 1st April 2023. Even if the notification is not made, s1018(4)(a) specifies that where the husband and wife live together for a tax year, they are deemed to have elected to be assessed under joint assessment.

Revenue Submission: Revenue stated that the appellant filed the return of income for the year 2023 on a separate treatment basis. Consequently, the appellant’s assessment for 2023 was determined under s1016. An election for joint assessment under s1018 and s1019 would not be allowed as the election was made after April 1, 2023.

TAC Decision: The TAC did not accept the appellant’s argument. Paragraphs 28 and 29 of the decision are very relevant. TAC interprets s1019 as the enabling section for applying the joint assessment under section 1017. According to the TAC, the requirement to provide notice before April 1 is mandatory for a taxpayer to apply for the joint assessment under s1017.

In my view, s1019 only enables the wife to become the assessable spouse. In fact, s1019(2) refers that the joint assessment under s1017 must be in effect for that year, either through an election under section 1018(1) or a deemed election under section 1081(4)(a). Therefore, even if the notification under Section 1019 is not made before April 1 of the tax year, and an election is made or deemed to be made under s1018, the husband and wife would be eligible for joint assessment under s1017, with the husband being the assessable spouse. Please refer now to the Appellant’s submission above for clarity. Additionally, paragraph 4.2.1 of the Revenue guidance indicates that the Revenue would automatically select the spouse with the higher income to be the assessable spouse. Consequently, the appellant should be allowed for joint assessment in the year 2023.

Please share your thoughts on this.